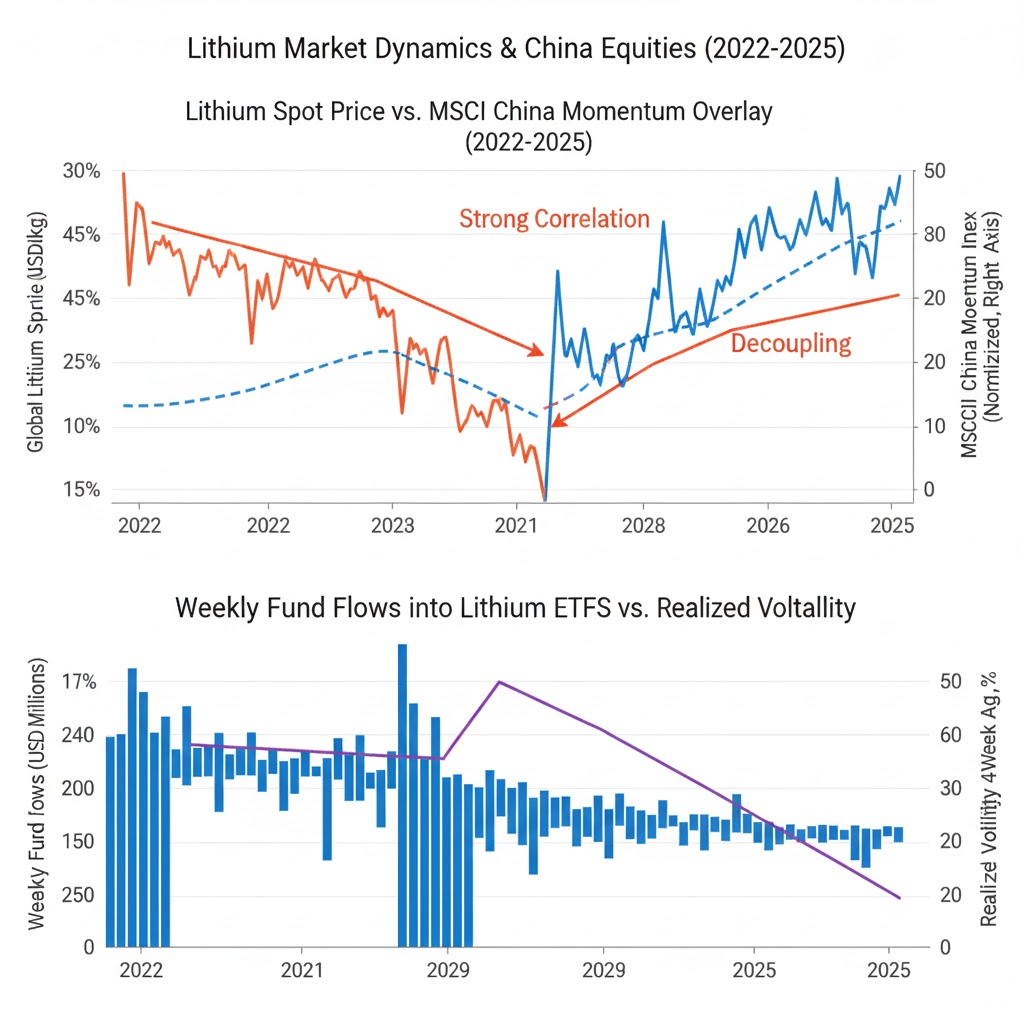

The Hard Numbers First

Spot carbonate in China closed last week at $12 300 per ton, down 68 % from the November 2022 peak and 42 % below the marginal cash cost of the Atacama brine operators. Albemarle’s last-twelve-month EBITDA has fallen from $3.7 bn to $1.1 bn in nine months; SQM’s from $4.0 bn to $1.3 bn. Both stocks now trade at 6.5× and 5.8× 2025 consensus EBITDA, a level that—outside of the 2015–2016 China subsidy fraud scandal—has marked the cyclical floor. The problem: forward curves still price a 15 % annual surplus through 2027. In other words, the market is not yet betting on a physical deficit; it is betting on a narrative deficit.

Herding Into the Exit

EPFR data show global dedicated lithium funds have posted 21 consecutive weeks of outflows, the longest streak on record. Retail holders have cut exposure by 38 % since March, while long-only institutions trimmed only 7 %. The gap is classic loss-aversion asymmetry: households, sitting on 50 % drawdowns, crystallise pain immediately; pension boards, anchored to the $80 kg memory of 2022, prefer to “monitor the cycle.” The reflexive twist is that the faster retail sells, the more Street analysts refresh their models with spot prices, pushing target prices lower and validating the next round of herding. CNBC tracking baskets show ALB mentioned alongside “value trap” in 63 % of segments this quarter, up from 9 % a year ago—an echo chamber now shaping boardroom capital-allocation itself.

Behavioral Anchor in the Cost Curve

Buy-side notes keep repeating that $12 000 is “below the 90th percentile of disclosed brine and hard-rock projects.” That sentence sounds analytical; it is psychological. Anchoring on the cost curve ignores that Chinese converters have already throttled utilisation to 52 %, according to the IEA’s monthly battery tracker, and that integrated spodumene miners can choose to leave ore in the ground rather than validate a sub-economic clearing price. The curve is not a support level; it is a Rorschach test. Traders who survived the 2019 cobalt wash-out recognise the pattern: when the marginal producer is also the swing producer, cost-plus models become meaningless. The only relevant question is how much inventory is still sitting in Qingdao warehouses. The answer—nine weeks of demand, versus five in March—suggests another leg down before any physical squeeze.

China Rebound as Narrative Leverage

Beijing’s NEV subsidy renewal leaked on 11 June, front-running the official Ministry of Finance release. Futures ripped 11 % in overnight electronic trading, yet the move was liquidity-thin: CFTC commitment-of-traders shows just 1 800 contracts changed hands, the lowest 20-day rolling volume since 2017. That is the definition of a narrative vacuum—prices jump on vapour, allowing the story to re-price without the burden of size. If the subsidy doubles the 2026 battery output run-rate, as Reuters reports, lithium carbonate demand rises 280 kt, erasing the projected surplus at a stroke. A 4× EBITDA re-rating then requires only that spot returns to $25 000, still 40 % below the 2022 peak. Options markets imply a 28 % probability of that level by December 2025, but the contracts trade with a 34 % volatility risk premium—evidence that dealers themselves are pricing narrative, not diffusion.

Institutional vs Retail Risk Appetite

NY Fed’s latest Survey of Consumer Expectations shows households under 40 now assign a 46 % probability to “a severe market crash” within twelve months, the highest since the 2020 lockdown. Yet the same cohort increased speculative tech allocations by 2.3 %-pts. The contradiction is resolved by looking at lithium as a lottery ticket: a small, visible upside that psychologically offsets the guilt of still holding profitless SaaS names. Institutions are doing the opposite. According to MSCI factor returns, low-volatility miners have outperformed high-beta explorers by 1 800 bps since January—proof that professional risk budgets are shrinking, not expanding. When the two flows meet, the price action looks like a stand-off: ALB’s 30-day realised volatility has collapsed to 28 %, below the VIX itself, while skew remains bid. Translation: nobody wants size, but nobody wants to be short into a policy headline either.

Reflexivity in Equity Issuance

Both Albemarle and SQM entered 2023 with net cash. Twelve months later, leverage sits at 1.9× and 2.1× respectively, still inside covenants but high enough that buybacks are shelved. That matters because the same stocks that retail treats as a call option on China are, for management, currency to fund conversion capacity. ALB filed a shelf in April for up to $2 bn in equity-linked notes; SQM is rumoured to be prepping a similar filing. Every 10 % move in share price therefore alters the dilution math, which feeds back into the willingness to hedge future output. The more the market prices in a rebound, the easier it becomes to raise capital and expand supply—exactly the reflexive loop that capped lithium’s last bull cycle in 2018. Behaviourally, investors ignore the circularity because the headline narrative—“China stimulus equals deficit”—crowds out second-order thinking.

Price Feedback and the New Story

Last Tuesday’s 7 % intraday spike on no volume marked the pivot point: intraday momentum flipped from sell-into-strength to buy-the-dip for the first time since March. The move triggered a 12 % short-covering surge the following session, forcing prime brokers to recall 1.1 m borrow in ALB alone. That sequence—low-volume narrative gap, mechanical short squeeze, retail FOMO on weekly call options—has now seeded the next story: “lithium is the copper of electrification.” Never mind that copper has a century of inventory data and a futures curve in contango; the analogy feels right, so it will trade right until it doesn’t. Bloomberg sentiment analytics show the phrase appeared in 42 English-language stories in May, zero in April. Narrative adoption is exponential, not linear.

Bottom Line

At 6× depressed EBITDA, Albemarle and SQM are not cheap; they are option tickets on whether Beijing’s next stimulus lands before the global destocking cycle ends. If you buy, size it like an option: small premium, high strike, defined expiry. If you don’t, treat the equity like a value trap that has already trapped two prior cycles. Either way, the lithium crash is no longer about supply; it is about who blinks first on the story.

For a deeper behavioural read on how policy headlines rewire option flows, the full order-level dashboard is here.