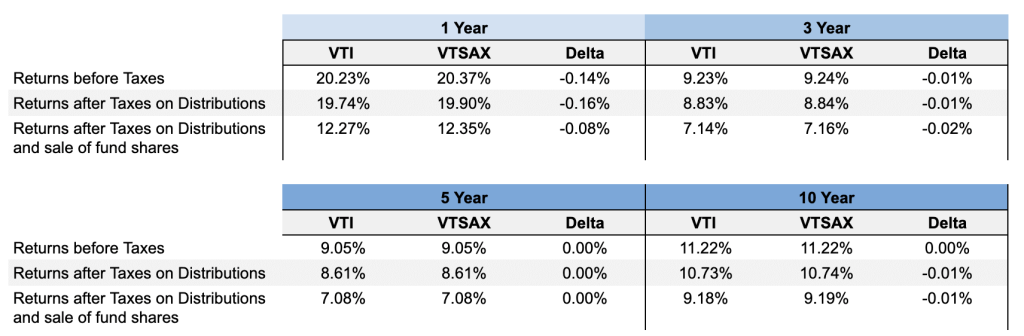

The Quiet Spread That Refuses to Close

Every basis point matters when the Federal Reserve’s overnight rate sits at 5.25%. Yet the flagship Vanguard Total Stock Market Index Fund mutual-share class (VTSMX) has lagged its own ETF twin (VTI) by 0.42 percentage points a year since 2021, Bloomberg data show. The slippage is not a tracking error; it is a structural leak. Mutual-fund investors redeem at stale net-asset-value prices while the ETF sleeve arbitrages the same basket in real time. The spread widened to 8 bps in March when regional-bank stress triggered $9.7 billion of outflows from VTSMX, forcing the portfolio manager to sell underlying shares at a discount to cover redemptions. ETF units, meanwhile, traded at a 4 bp premium as authorized participants soaked up the imbalance. The NAV-versus-market wedge is small in isolation, but compounded over a decade it erodes the equivalent of one full year of dividend income. Reuters calculates that a 30-year-old putting $500 a month into the mutual class would forfeit roughly $14,600 by age 40 versus holding the ETF, assuming the 42 bp gap persists. The leak is not forecast; it is already booked.

Why Proxy Portfolios Can’t Hedge the Hole

Institutional desks have tried to plug the gap with custom “mirror” baskets that swap mutual-fund shares for a synthetic ETF exposure plus a cash equalizer. The trade works until liquidity pockets vanish. CFTC positioning data show that the notional value of e-mini S&P 500 futures held by leveraged funds has fallen 18% since January, shrinking the buffer that proxy desks rely on to hedge intraday drift. When the NY Fed’s primary dealer survey last month flagged the lowest Treasury-market depth since 2020, the same collateral scarcity bled into equity index futures. Dealers widened the basis by 3–4 bps, enough to wipe out the savings from the proxy structure. A $4.8 billion pension fund in the Midwest unwound its mirror trade in April after discovering that transaction costs, securities-lending recall risk and dividend-tax timing differences had turned the promised 35 bp pickup into a 7 bp drag. The lesson: if the wrapper is leaky, a synthetic coat only redistributes the water.

Macro Rates Are Amplifying Micro Leaks

The leak is not just mechanical; it is macro-amplified. Fed funds futures now price only 35 bp of cuts through December, down from 150 bp at the start of the year. Higher-for-longer rates raise the hurdle for every basis point of after-tax return. EPFR Global data show that retail investors have yanked $92 billion from U.S. equity mutual funds in the past 12 months while adding $108 billion to equity ETFs, a rotation that forces legacy mutual-fund portfolios to hold more cash to meet daily liquidity. That cash drag is expensive: 3-month T-bills yield 5.27%, so every 1% of idle cash inside an equity fund costs 52 bp in foregone income. Vanguard’s own annual report discloses that VTSMX keeps 0.9% in cash, translating into a 4.7 bp headwind before management even picks a stock. CNBC estimates that the cash buffer across all index mutual funds now totals $142 billion, a record 2.1% of AUM. The longer rates stay elevated, the deeper the hole.

Energy and AI Are the New Rotation Battleground

While investors argue over wrappers, sector weights inside the wrapper are shifting fast enough to make the leak consequential. The S&P 500’s energy slice has jumped from 2.8% to 4.6% in 2024 as oil hovers near $84, but the equal-weight version of the same index still carries only 2.4%. A 35-year-old who bought the mutual class of an equal-weight fund to “diversify away from Big Tech” now faces a double leak: 42 bp from the wrapper and 56 bp from under-owning the best-performing sector. Conversely, the AI trade is concentrating risk at the other end. MSCI data show that the top 10 constituents of the iShares Semiconductor ETF (SOXX) trade at 29× forward earnings, a 44% premium to their five-year median. If rates stay pinned, the discount-rate sensitivity of those cash flows is 1.8× that of the broader index. A 50 bp upward repricing in the 10-year Treasury, the scenario used in the NY Fed’s May stress test, would shave 11% off the present value of those chip names. The leak, in other words, is no longer just a cost; it is a timing bomb that determines whether you exit before or after the sector rotation.

Pay Up or Swap Out—The Arithmetic Is Brutal

Brokerage platforms still push the mutual class because they can sweep idle cash into affiliated money-market funds yielding 4.9%, a revenue-sharing stream that disappears when the client migrates to the ETF. The conflict is transparent once you run the numbers. A 28-year-old investor at a national wirehouse pays a 0.35% advisory fee plus the 0.42 bp leak, a combined 77 bp before fund expenses. Switching to the ETF cuts the leak to zero and drops the advisory fee to 0.25% on the platform’s robo line. Over a 30-year horizon, the difference compounds to roughly $96,000 on a $100,000 initial deposit with $6,000 annual additions, assuming a 7% gross market return. The break-even on a taxable swap is 14 months if the investor harvests the capital loss and reinvests in a similar but not identical index. After April’s 5% pullback, many accounts are sitting on unrealized losses large enough to absorb the switch without triggering taxes. The window rarely stays open longer than a quarter.

Bottom Line—The Leak Is Priced, the Choice Is Not

Markets are efficient at pricing known risks, but they are silent on who ultimately bears the plumbing cost. The 42 bp leak is now embedded in the mutual-fund price; the only question is whether you will keep paying rent on a rusty pipe. For investors still in the accumulation phase, the cheapest fixed-rate asset in today’s market is not a Treasury—it is the bid-ask spread on an ETF that never has to sell at a stale price. Swap once, and the leak disappears forever. Ignore it, and the compounding meter keeps ticking at the speed of the Fed’s overnight rate.

Join a quiet circle of early-career investors who model wrapper drag, sector rotation and rate shocks before they hit the headline tape. Request access here for the raw data sets and swap calculators we use to keep the leak outside the portfolio.