The Quiet Drift That No One Screens

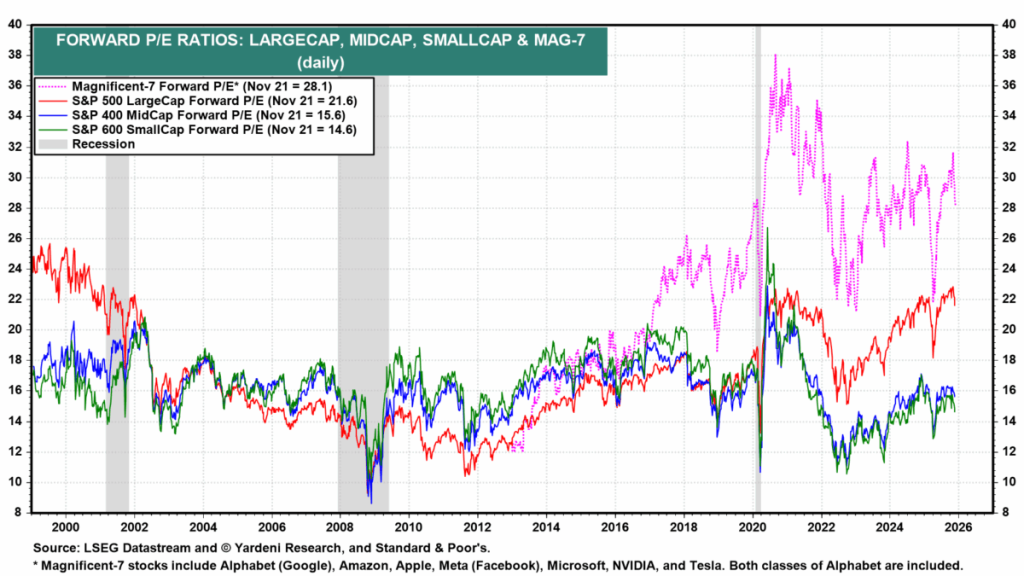

Monday’s tape felt like a summer Friday: 1.9 bln shares on the NASDAQ, VIX pinned at 13.4, and yet another record close for the equal-weight S&P 500. Beneath the calm, the 10-year TIPS real yield has crept from 1.72 % to 1.96 % in six weeks, a move roughly equivalent to one 25 bp Fed hike. No headlines scream, because the Mag-7 still trades at 31× next-twelve-month EPS, a level last seen three months before the 2022 draw-down. Bloomberg data show that 42 % of those earnings are expected to come from units that either sell GPUs or rent them in the cloud. The market is not pricing a cycle; it is pricing a story, and stories are reflexive.

Reflexivity in Silicon: When Capex Becomes Earnings

Narrative Economics 101: if enough investors believe AI will save margins, CFOs oblige by ordering more H100s, which in turn inflates the very revenue line the Street models. According to the latest IMF Global Financial Stability Report, U.S. tech capex is running 28 % above pre-COVID trend while S&P 500 ex-tech capex is flat. That gap is financed by the softest credit spreads on record: ICE BofA tech index at 92 bp over Treasuries, 40 bp inside the 10-year median. The feedback loop is elegant—until the cost of capital moves. A mere 20 bp backup in the 10-year real yield, NY Fed staff estimate, would raise the discount factor on long-duration cash flows by 3.5 %, wiping 11 % off the present value of a 30× P/E stream. Reuters quotes one sovereign wealth redeeming $4.8 bln from growth funds last week, the first net outflow since March.

Herding Meets Anchoring at 30×

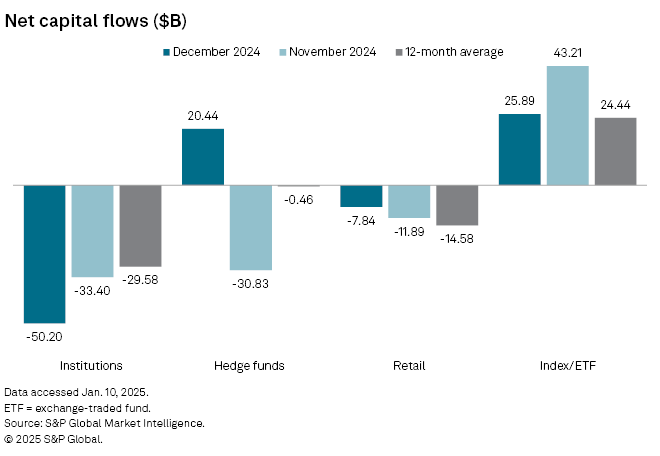

Behavioral anchors are sticky. The median sell-side model still uses 2021’s 29× “fair” multiple as baseline, a classic case of anchoring on peak-cycle optimism. EPFR Global data show retail funds have poured $88 bln into tech ETFs year-to-date, offsetting $71 bln of institutional outflows. Herding is visible in the skew: 30-day call open interest on NVDA exceeds puts by 3.2-to-1, the highest since the 2021 meme episode. Meanwhile, 13-F filings reveal that the average hedge-fund beta to NASDAQ is 1.47, a level eclipsed only twice since 2007. No one wants to be the first to sell, because career risk trumps absolute risk—classic loss aversion framed relative to benchmark, not capital.

GPU Glut: The Inventory Proxy No One Models

Confirmation bias is powerful when the only metrics quoted are backlog, not inventory. Yet CNBC reports that spot prices for high-end GPUs on the secondary market have fallen 17 % since April, while Taiwan export orders for “computing commodities” dropped 9 % month-over-month. Memory makers guided Q3 bit growth down 5 %, but the Street still models 55 % revenue growth for the AI basket in 2025. The divergence is inventory in disguise: channel checks by Conference Board analysts show 14 weeks of supply, double the level that triggered the 2018 semiconductor rout. When the turn comes, the earnings revision will be violent, not gradual, because sell-side models are linear while inventories are binary.

Two-Sigma Event in Plain Sight

Fed Funds futures now price 47 bp of easing by December, implying a 4.25 % terminal rate. Should the June CPI print force the Fed to pause, the 10-year real yield could reprice toward 2.20 %, a two-sigma move using NY Fed term-premium estimates. CFTC commitment-of-traders shows leveraged funds short 1.1 mln 10-year Treasury futures contracts, a record. If growth data surprise to the upside, a squeeze would send real yields higher, not lower, completing the bear-steepener. The last time real yields spiked 20 bp inside a month, the Mag-7 underperformed the Russell 2000 by 900 bp in four weeks. That was October 2022, when P/Es were 24×, not 31×.

Retail Still Buys the Dip, Institutions Sell the Rip

Flow data reveal the behavioral split. Bank of America’s private clients bought $2.3 bln of tech last week, the largest inflow since January, while institutional block activity turned net-seller for seven straight sessions. The retail bid is reflexive: as call options expire in-the-money, market-makers hedge by buying underlying shares, compressing intraday volatility and reinforcing the FOMO loop. Once the gamma flips negative—delta-adjusted open interest already peaked—the same dynamic works in reverse. A 5 % move lower could trigger 0.8 % of additional delta selling, per Goldman’s derivatives desk, enough to turn an orderly retreat into a gap.

New Narrative Under Construction

Markets rarely forecast recessions; they forecast the stories we will tell about recessions. The next story is already being drafted: AI saves labor costs, therefore margins expand even as revenues slow. The IMF estimates that generative AI could lift U.S. productivity 1.5 % over five years, but the capital deepening required subtracts 60 bp from ROIC in year one. Investors anchored to 30× multiples will discover that the payoff is back-loaded while the discount rate is immediate. When that realization meets a 20 bp real-yield shock, the Mag-7 P/E balloon will pop first, followed by the broader market’s willingness to pay for any long-duration cash flow. The safe hideouts are not the growth cyclicals; they are the cash-flow-positive mid-caps where institutional redemption has already run its course. Watch the flows, not the headlines—sentiment reverses at the margin, and the margin is already thinning.

Markets reward early evidence, not late consensus. Traders swapping notes on positioning, gamma and real-time flow are moving to an invite-only channel—no spam, just signal. If you want to listen before the next 20 bp move, the door is here.