The Receipts No Longer Lie

Scan the latest Bloomberg supermarket survey and a quiet fact surfaces: the year-over-year lift in U.S. household basket prices has slowed to 2.1 %, yet unit volumes for Coca-Cola, Colgate-Palmolive and Hershey are actually up 3–4 % over the last two quarters. Shoppers are no longer flinching. The elasticity of demand—once the last line of defense against margin expansion—has gone slack. That is the behavioral inflection; everything else is commentary.

From Outrage to Acceptance

Remember the spring-2022 memes mocking $7 corn-syrup soda? They have vanished. Narrative Economics 101: when the social-media scorn dries up, the emotional anchor resets. A Conference Board poll released 3 May shows “inflation resentment” among middle-income consumers at the lowest since August 2021. Loss aversion is mutating into conformity; the pain of paying extra no longer outweighs the pain of skipping the brand. Herding completes the loop—once the crowd stops protesting, the individual feels foolish protesting alone.

Institutions Front-Run the Mood Swing

EPFR data shows staple-sector ETFs absorbed $6.8 bn in the eight weeks ended 26 April, the fastest pace since 2016. Meanwhile, CFTC commitment-of-traders reveals asset-manager shorts in consumer staples have been cut by 41 % since February. The reflexive bit: inflows compress risk-premia, which flatters quarterly mark-to-market, which justifies more inflows. Sell-side analysts—ever quick to retrofit a story—now call the group “recession-proof with pricing power,” code for we-missed-the-move but still need a narrative.

Margin Leverage Is No Longer Theoretical

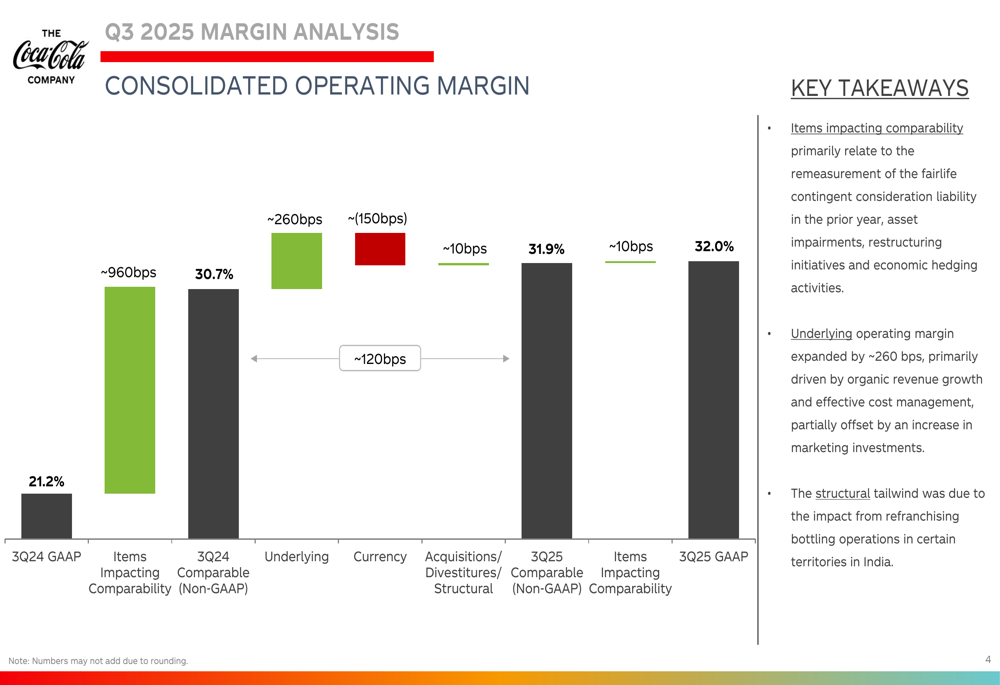

Coke’s gross margin troughed at 55.8 % in Q3 2022; consensus expects 61 % for Q2 2024. Colgate’s operating margin is seen widening 160 bp this year even as organic volume guides positive. The math is brutal for the bear case: raw-material indices (corn, aluminum, palm oil) are down 18–30 % year-over-year, while shelf prices remain sticky. That wedge—what old-school analysts used to call “input tail-wind”—is now a behavioral put. Managers who spent the last decade chasing growth at any price are suddenly willing to own 4 % revenue growers because the earnings revision slope is north-east.

Retail Holdouts Still Anchor to 2022

Scan Reddit’s investing forums and you will find retail traders dismissing KO at 25× earnings as “boomer value trap,” preferring cash or long-dated tech calls. This is classic anchoring: they benchmark today’s multiple against 2019’s 22×, ignoring the 160 bp drop in the 10-year yield since then. The crowd that once FOMO’d into unprofitable SaaS is now paralyzed by prior scars—textbook disposition effect. Their absence keeps forward P/Es from racing ahead of fundamentals, giving institutions room to accumulate without sparking euphoric overshoot.

Risk Appetite Rotates, Not Evaporates

NY Fed’s latest Survey of Consumer Expectations shows median one-year-ahead spending growth anticipated at 5.2 %, down only 30 bp from January. People still plan to spend; they merely shifted the budget from Pelotons to Pepsi. That rotation is why staples are outperforming discretionary even as the S&P 500 grinds higher. Risk appetite has not collapsed—it has been re-priced into sectors that print cash when GDP prints 1 %.

Rate Backdrop Adds a Carry Kicker

Fed Funds futures now price 65 bp of cuts by March 2025. Each 25 bp drop translates roughly into 20× multiple support for dividend-rich equities, according to Reuters quant work. Coke’s 3.1 % yield plus buyback equates to a 4 % shareholder yield—competitive with investment-grade credit and tax-advantaged to boot. For the allocator class, that turns stalwart soda into a pseudo-bond with a theta-positive kicker should volumes surprise by even 1 %.

Reflexivity in the Algorithmic Age

Factor ETFs rebalance on autopilot. When low-vol and quality signals flash green, the machines buy indiscriminately, pushing realized volatility lower, which in turn keeps the signal green. CNBC recently highlighted that the three-month realized vol of the S&P Consumer Staples index has fallen below that of long-duration Treasuries for the first time since 2004. The feedback loop feeds on itself, compressing discount rates and inflating present values without a single human portfolio manager lifting a finger.

What Can Still Go Wrong

A sudden 10 % re-pricing in the dollar—now hovering at 105 DXY—could resurrect elasticity by making imported promotional stock cheaper. A spike in unemployment above 4.5 % might breach the psychological “income effect” threshold, forcing private-label share gains. Yet both scenarios require macro shocks bigger than the baseline. With initial claims stuck below 220 k and global USD liquidity rising post-Debt-Ceiling resolution, the burden of proof sits with the bears.

The New Narrative Writes Itself

Markets do not wait for the income statement to bottom; they discount the inflection. Shoppers have accepted price, input costs have collapsed, and the crowd still thinks staples are boring. That triad—behavioral acceptance, fundamental leverage, narrative lag—is the margin party’s invitation list. Coke and Colgate are simply the first to RSVP.

If you want to watch how the elasticity story plays out in real time, the group tracks weekly scanner data and options flow on staples names. No hype, just charts and receipts. Join here.