The Commission Chasm Opens

Last month a midsize Midwest broker emailed clients a line that would have sounded like a prank in 2019: “Execute any buy order in our curated ETF list and we will credit your account one basis point.” The firm is not charitable; it is surviving. Bloomberg reports that the aggregate expense ratio collected by the top-five exchange-traded product sponsors has fallen thirty-eight percent since 2021, while payment-for-order-flow rebates have compressed by half. The economics of simply holding customer cash now eclipse the economics of executing the trade, so the ticket itself becomes a loss-leader. That is the fact. The emotional fallout is more slippery.

Retail investors, conditioned by fifteen years of zero-commission rhetoric, interpret the credit as confirmation that trading is now risk-free. Anchoring to the old “$7.95” round-trip cost has not disappeared; it has merely collapsed toward zero and kept moving. When the platform pays you, the brain records a gain before the position is even chosen, short-circuiting loss-aversion circuitry that once made investors pause. The result is a measurable uptick in what behaviorists call “lottery seeking”: small-ticket, narrow-niche ETFs with three-figure expense ratios are seeing record creations even as their underlying baskets underperform by triple that fee. The credit is one basis point; the behavioral drag can be one hundred.

Herding into the Rebate Trap

Institutional desks are not immune. Asset allocators who would blush at admitting they chase rebates have simply cloaked the impulse inside a narrative about “best execution.” Reuters details how three large registered investment advisers moved $4.7 billion of model-portfolio trades to a newcomer platform that guarantees negative commissions. The platform recoups the cost by internalizing flow and selling real-time data back to the very market makers providing the rebate. Reflexivity enters: the more size the RIA directs, the tighter the spread becomes, the more attractive the venue looks, the more flow it attracts. Price becomes the marketing budget, and the feedback loop masquerades as efficiency.

Meanwhile the end-investor—often a 401(k) participant in a target-date fund—believes the fiduciary is shopping for the cheapest beta. In reality the fiduciary is harvesting a micro-subsidy that belongs to the beneficiary, converting it into soft-dollar research credits and conference fees. The herding is vertical: retail buyers chase issuers, issuers chase flow, advisers chase platforms, all because the minus sign in front of the commission feels like found money.

Confirmation Bias Meets Distribution Yields

Negative commissions arrive just as cash yields five percent. The contrast turbo-charges confirmation bias: “If I can get paid to trade and my idle cash earns five percent, any equity position only needs to avoid a major drawdown to win.” The mental math is dangerously tidy. CNBC quotes a Bay Area engineer who swapped his monthly dividend-ETF drip into a 0.95%-expense thematic cloud fund that rebates half a basis point. He cheerfully concedes the fund lags its benchmark by 1.3% annually, but the rebate plus money-market yield “feels like a hedge.” That is textbook disposition effect: the investor over-weights the realized credit and under-weights the unrealized erosion, because the credit is visible today while underperformance is deferred.

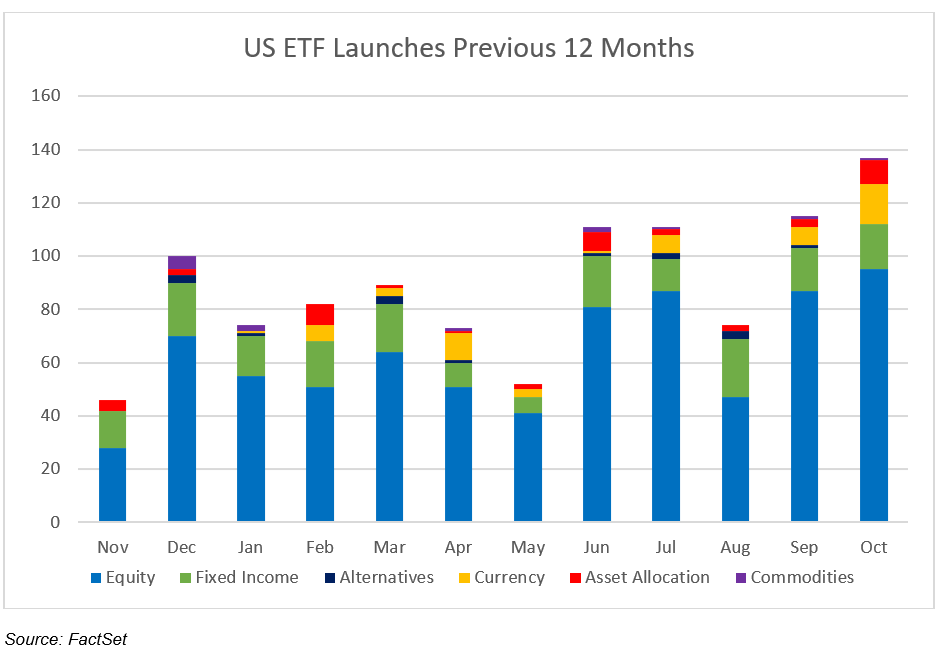

The same psychology is showing up in option-overlay ETFs that distribute twelve percent while truncating upside. Flow data from Morningstar show net creations of $28 billion this year in covered-call products, the fastest pace on record. Investors are not buying equity exposure; they are buying the story of “income that beats cash,” and the negative commission is the ribbon on the package. The narrative is so potent that even a modest summer pullback in the Nasdaq could trigger a reflexive unwind: dealers who sold the calls will be forced to buy back deltas, amplifying volatility just as the income story fractures.

Risk-Appetite Divergence Across Ages

Behavioral finance often treats investors as a monolith, but the rebate era is splitting them by birth year. Accounts opened since 2020 trade 3.4 times more frequently when the ticket is credited, according to a Schwab white paper, yet accounts opened before 2008 show no change in turnover. The older cohort still anchors to the memory of paying for execution; the younger cohort anchors to being paid. The split has asset-allocation consequences. Dividend aristocrat ETFs—whose median holder is fifty-four—have seen outflows for six straight weeks, while zero-commission thematic funds with negative fees skewed to investors under thirty-five pull in fresh money every Friday, the day most platforms sweep excess cash into purchasing power. The risk-appetite thermostat is calibrated not by volatility but by the sign in front of the commission.

Where the Pendulum Snaps Back

Every race to zero ends the same way: someone starts charging for something else. In 2009 it was payment for order flow; in 2024 it is real-time behavioral data. Platforms that pay you to trade are not charities; they are arbitraging the gap between your latent attention and the advertiser who will pay for it. The moment custodial cash yields dip below three percent, the credit will disappear, and the same investors who felt thrilled to earn one basis point will face the mirror image of loss aversion: a sudden reintroduction of cost. History suggests turnover will fall by half within a quarter, liquidity will gap, and the very ETFs that benefited from the rebate will face redemptions at the same time. The narrative will flip from “paid to trade” to “pay to exit,” and the reflexive spiral will run in reverse.

Until then, the smart play is to separate the signal—lower frictions are structurally bullish for long-term share ownership—from the noise of negative commissions. Use the credit to average into broad, low-cost dividend ETFs whose brand is not built on the rebate, and treat any thematic trade that needs the credit to justify itself as a warning label. The market is not paying you to invest; it is paying you to behave. Make sure the behavior you choose still makes sense when the check stops coming.

For readers who track how micro-incentives reshape macro-flows, extended behavioral-finance notes are posted weekly via this link.