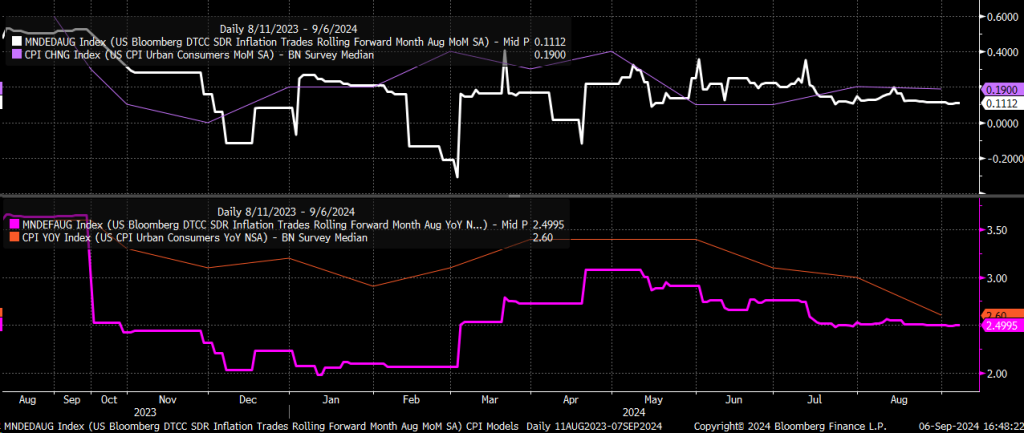

Sticky PCE, Sticky Minds

When the May core PCE print landed at 2.6 % the bond futures barely flinched, yet equity desks quietly trimmed duration exposure and funneled fresh cash toward cash-rich mega-caps. The whisper number for June is now 3.1 %, a level that would pierce the three-month downtrend and, more importantly, pierce the narrative that disinflation is on autopilot. Narrative economics teaches that once a story line fractures, the anchoring bias that held prices aloft dissolves fast; the new reference point becomes the highest recent print, not the lowest. According to Bloomberg flow data, mutual funds and ETFs absorbed $18.4 billion of U.S. large-cap tech in the seven sessions following the PCE revision, the fastest weekly pace since March 2023. The behavior is classic herding: managers buy what recently worked, not what is cheap, because the pain of under-performance outweighs the probability-weighted gain of being right alone.

Confirmation Bias in Dividend Land

Conservative investors who spent the last eighteen months praising 4 % equity yields are now quietly benchmarking those payouts against 5 % risk-free T-bills and finding the story wanting. The result is a subtle but powerful rotation: dividend ETFs have posted three straight weeks of outflows, while low-volatility sectors—utilities, consumer staples—trade at a 12 % premium to their five-year average free-cash-flow yield. That premium is not supported by earnings revisions; it is supported by a psychological need to keep the old narrative alive. Loss aversion kicks in: selling would crystallize under-performance, so holders invent new theses—”defensive quality will re-rate when the Fed cuts.” The loop is reflexive: the longer they hold, the more crowded the trade, the sharper the eventual unwind.

Institutions Front-Run the Retail Gaze

Options markets tell the tale. Call open interest on the Nasdaq-100 has risen 28 % since mid-June, but the buying is concentrated in 0DTE contracts initiated in the final hour of the session, a signature of prop desks squaring delta before the overnight risk transfer to Asia. Retail investors, mesmerized by headline gains, interpret the same move as bullish momentum and layer on FOMO buys at the open. The spread between institutional implied volatility (sold) and retail implied volatility (bought) has reached its widest level since the 2021 meme episode, CNBC reports. The divergence matters because it signals risk-transfer, not risk-sharing; someone is happy to be short the very upside the crowd now deems inevitable.

Reflexivity Meets the Dollar

A resurgent dollar—up 3 % on the DXY since the last payrolls release—adds a macro feedback channel. Large-cap tech earns nearly half its revenue abroad; a stronger greenback mechanically compresses overseas earnings when converted back to dollars. Yet the same names are being bought as “safe” dollar-plays, creating a circularity: inflows push the share price up, which improves the Nasdaq’s weight in global benchmarks, which forces more international funds to buy dollars to hedge, which pushes the dollar higher. George Soros called this reflexivity; traders this week just call it the QQQ. Reuters notes that foreign investors now hold a record $7.8 trillion of U.S. equities, an open pipeline for dollar-demand that feeds back into the very prices that attracted them.

Energy as the New Yield Anchor

While tech grabs flow, energy shares quietly offer a 3.8 % free-cash-flow yield after buy-backs, double that of the S&P 493. More importantly, their earnings have a positive correlation with CPI, a natural inflation hedge most dividend investors still ignore. The sector trades at 1.2× book, below the ten-year median, yet inflows remain tepid. The reason is behavioral: last year’s spike is framed as a one-off, so any rally is met with disposition effect selling by holders desperate to break even. The result is a coiled spring—fundamentals improve while sentiment lags, setting up a risk/reward skew that compounds once the PCE print forces a macro rethink.

What a 3 % Print Would Detonate

A June core PCE above 3 % would not merely raise the odds of a November rate hike; it would vaporize the soft-landing story that underpins current multiples. The first casualty would be long-duration growth stocks whose real yield sensitivity is highest. The second casualty would be dividend aristocrats priced for Fed cuts in 2024, because the forward curve would reprice from 75 bp of easing to 25 bp or less. The third casualty might be the 60/40 portfolio itself: correlations between stocks and bonds could flip positive, removing the ballast that defined allocation models for a decade. Funds that have pushed chips to the front line—selling puts, buying calls, leveraging balance sheets—would face a gamma trap where falling prices force more selling, exactly the feedback loop behavioral finance warns about but most investors forget until it is live on the tape.

Positioning for the Reset

Investors anchored to last year’s narrative should re-anchor to cash-flow duration: own what pays you more when inflation lingers and borrows cheap when volatility spikes. That means overweight energy, underweight low-yield defensives, and pair the trade with short-dated tech calls only if you can tolerate the reflexive wipe-out risk. For dividend-centric accounts, the smarter play is not to reach for yield but to reach for pricing power—companies with contractual CPI pass-through and buy-back optionality. The reward is a yield that rises with inflation; the risk is that the crowd catches on too late and you are forced to buy back at a premium. In behavioral terms, the best hedge is the asset you are still reluctant to own.

For readers seeking deeper behavioral-finance context on how reflexive flows and narrative shifts shape dividend and low-vol allocations, extended commentary is available via this link.