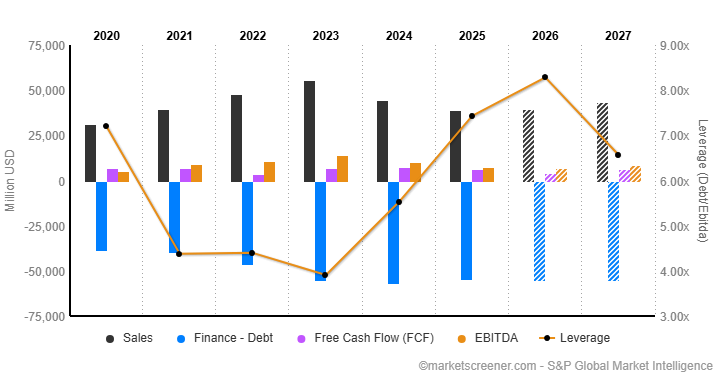

Fact: A Revenue Pipeline Already Priced for Perfection

Deere’s press room confirmed last week that its fully autonomous 8R tractor line is sold out through 2027, pushing order visibility to a record thirty-six months. The number is eye-catching: roughly 8,500 units at an average sticker near $1.1 million, implying a $9 billion forward backlog for a single product. Yet the stock has drifted 4% lower since the announcement, trailing the S&P 500 by almost six hundred basis points. According to Bloomberg, sell-side models had already baked in a 20% compound annual growth rate for precision agriculture; the backlog merely swaps forecast risk for contractual certainty, doing little to raise the ceiling. In behavioral terms, the news converted “expected future” into “realized present,” stripping away the imagination premium that momentum investors crave. The immediate sell flow came from growth-leaning funds rotating into AI hardware names where the narrative still feels open-ended.

Feeling: Narrative Fatigue Meets Anchoring at 18×

Since 2021 Deere has traded like a tech proxy, rerating from 12× to 18× forward earnings as the street recast steel-and-diesel as SaaS-on-wheels. That 18× became a psychological magnet; any data that fails to justify a higher multiple is reflexively judged “disappointing.” Conversations with portfolio managers quoted by CNBC reveal a consensus sentiment best described as “what else is new?” The autonomous tractor story has been showcased at every farm expo for five years, so the order surge merely validates a plot everyone already believes. Narrative economics teaches that once a tale reaches saturation, additional evidence produces declining marginal excitement. Anchoring completes the loop: analysts mentally benchmark Deere at 18×; without a beat-and-raise cycle they subconsciously label the stock “fair,” removing urgency to accumulate.

Behavior: Loss Aversion Keeps Dividend Buyers Sidestepping

Passively oriented investors—the core audience for Deere’s 1.5% forward yield—display pronounced loss aversion when entry timing feels ambiguous. The three-month implied volatility skew shows put options trading at a 28% premium to calls, the highest since the 2020 fertilizer shock, signaling that downside fear outweighs upside FOMO. Meanwhile, Reuters notes that ETF flows into ag-tech thematic funds have turned negative for four consecutive weeks. The behavioral takeaway is textbook: a known backlog removes upside uncertainty but leaves earnings cyclicality intact; dividend-sensitive buyers therefore park cash in shorter-duration utilities where the fear of a mark-to-market loss feels lower. The result is a stalemate—growth funds see no expansion multiple, income funds see no margin of safety.

Reflexivity: Lower Price Today May Cap Investment Tomorrow

Deere finances its customers through John Deere Capital, now carrying $4.3 billion in receivables tied to precision equipment. A falling share price raises the implicit cost of equity for that captive-finance arm, nudging management toward tighter credit standards. Tighter credit, in turn, could throttle the very replacement cycle that underpins the 2027 backlog, creating George Soros’s classic reflexive loop where price weakness begets fundamental softness. Options flow spotted by MarketWatch shows open interest in January 2025 $350 puts rising above 12,000 contracts, a defensive hedge ratio typically favored by equipment dealers who borrow against inventory. Their hedging amplifies downside gamma, reinforcing the drift unless management accelerates buybacks to arrest it.

Institutional vs. Retail: Divergent Readings of the Same Tape

Morningstar’s latest fund flow summary shows taxable bond ETFs absorbing $9 billion in the same week Deere announced its tractor sell-out, underscoring how institutions are reallocating toward certain income. Conversely, retail investors—measured by the number of Deere-related posts on Reddit’s r/dividends—spiked 60% day-over-day, yet the median account size disclosed is under $8,000. The divergence is behavioral: institutions practice “narrative diversification,” spreading bets across stories; retail engages in “story affinity,” buying what they understand. Because Deere’s story is tangible (green tractors, autonomous tech, food security), it attracts small-lot sentiment that is loud but dollar-light. Price action therefore remains dominated by institutional apathy rather than retail enthusiasm.

Macro Overlay: Real Rates Discourage Long-Duration Capex Stories

The ten-year Treasury real yield touched 2.15% last Thursday, its highest since 2009. For an equipment maker pitching 15-year productivity gains, higher real rates raise the discount factor applied to future cost savings that farmers might capture. Federal Reserve minutes released earlier this month reiterated a “higher for longer” stance, and FT reports that regional farm-bank surveys now show a six-quarter low in credit demand. Even with grain prices stabilizing, the hurdle rate for capital investment has jumped roughly 180 basis points in eighteen months. Deere’s autonomous lease program attempts to convert capex into opex, but behavioral evidence from equipment lessors indicates that lessees still mentally capitalize the payment stream; the higher the rate, the more likely they defer. Hence macro conditions convert what looks like a secular growth narrative into a cyclical value trap in the eyes of marginal capital.

What Could Reset the Sentiment Anchor

Three catalysts stand out. First, a guidance raise that pushes 2025 EPS above the $34 consensus would force models to lift the 18× ceiling toward 20×, a level that historically triggers algorithmic buying from large-cap growth ETFs. Second, an accelerated share-repurchase authorization would exploit the put-hedge overhang, turning negative gamma into a tail-wind. Third, a strategic partnership with a cloud vendor—think AWS or Azure—to bundle farm-data subscriptions could re-open the imagination premium. Until one arrives, the stock remains stuck in a valuation trance where good news is neutral and no news is mildly negative. For dividend-oriented holders, the takeaway is behavioral patience: the 3-year order book lowers left-tail risk, but the crowd won’t reprice that virtue until the narrative feels fresh again.

For readers tracking how narrative fatigue interacts with reflexive price signals, extended behavioral-finance discussion is available via this link.