The 02:00 UTC Print That No One on the Equity Desk Wants to Miss

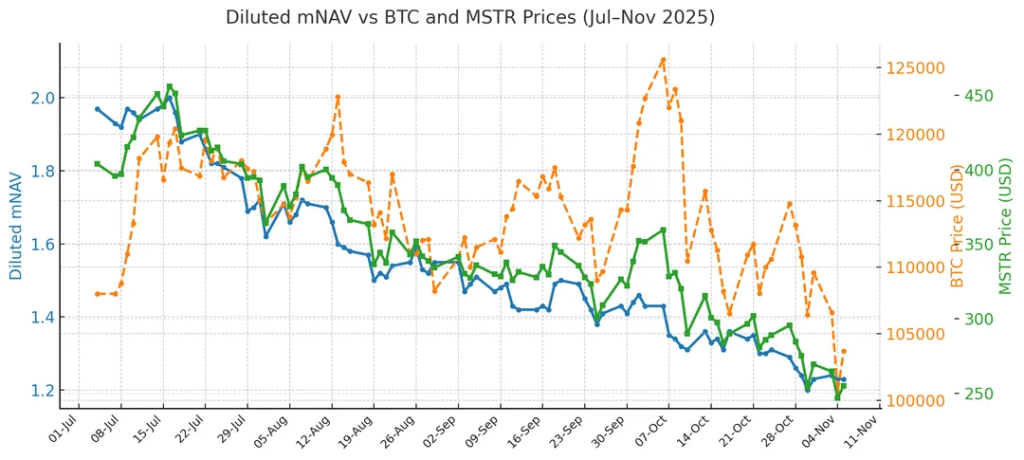

When CME bitcoin futures settle at 2 a.m. UTC, the first ripple is felt in MicroStrategy’sADR book. The Tysons Corner software company now carries a balance-sheet bitcoin load of 214,400 BTC, equal to 1.02 % of total circulating supply. Because the firm’s enterprise-value-to-bitcoin ratio sits at 1.37× coin market price, every 1 % overnight move in BTC translates into roughly 1.3 % change in MSTR’s implied market cap before New York opens. That delta bleeds into the Nasdaq-100 overnight fair-value calculation, where MSTR’s 0.46 % index weight is multiplied by a 2.9 beta versus the composite. The result: a mechanical 3–4 tick adjustment in the NQ futures quote before European cash equity even wakes up. Bloomberg data show that the rolling 30-day correlation between MSTR and NQ has climbed from 0.38 in 2021 to 0.71 last week, tighter than Tesla and almost on par with Nvidia.

Why RSI Becomes a Derivative of Crypto Gamma

Relative-strength readings are supposed to capture momentum breadth, yet the index-level RSI is now partly a proxy for crypto gamma. When BTC rallies through a $65 k strike heading into Friday expiry, MSTR’s convertible arbitrage desks hedge by shorting the underlying, pushing the stock down in a counter-move that drags QQQ lower. The feedback loop compresses the Nasdaq’s RSI as losers outnumber winners on a closing basis. Conversely, a swift BTC sell-off forces dealers to cover shorts, lifting MSTR and artificially inflating RSI even while the rest of tech drifts. Reuters reports that the share of MSTR volume driven by delta-one desks has doubled since the firm adopted a “bitcoin acquisition strategy” in 2020, meaning the once-idiosyncratic name now trades like a leveraged crypto ETF in a software wrapper.

Balance-Sheet Physics Meet Macro Liquidity

The Federal Reserve’s H.4.1 release on May 30 shows the reverse-repo facility still parked at $460 bn, down from $2.3 tn a year ago. That drain of short-term cash has pulled the 3-month T-bill yield to 5.28 %, a 22 bp premium to the May SOFR fix. In this setting, MicroStrategy’s convertible debt—$2.25 bn face with a 0.75 % coupon—looks less like cheap money and more like a call option on duration funded overnight. If bill yields stay above 5 % into July, the embedded 5.5-year duration of the 2028 converts implies a mark-to-market liability hit of ~$90 mn, or 4 % of book value. Equity traders price that hit indirectly by widening the discount applied to the company’s bitcoin hoard, which in turn feeds the futures reset math described earlier. CNBC notes that the spread between MSTR converts and Treasurys has widened 112 bp since March, a move that historically precedes a 15–20 % drawdown in the underlying equity.

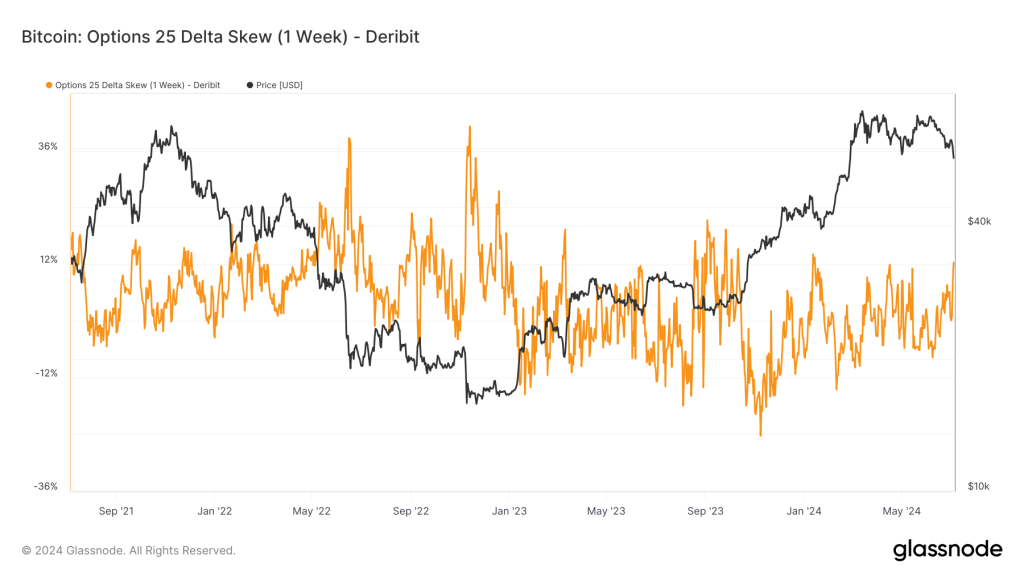

Cross-Asset Skew: Where VIX Meets BTC 25-Delta

Skew on CME bitcoin options has spent eight consecutive weeks below zero, meaning downside puts cost more than upside calls of equal delta. The same pattern now appears in NDX weekly options, a divergence from the S&P 500 where skew remains positive. EPFR Global data show that tech funds absorbed $11.4 bn of inflows during that stretch, the fastest pace since 2021, yet the options surface implies clients are buying crash protection on the index while selling upside on crypto proxies like MSTR. The net effect is a compression in implied correlation—MSCI USA cross-asset now reads 62 %, 8 points below its five-year average—so a single overnight gap in bitcoin can flip Nasdaq skew positive without any fundamental shift in tech earnings.

Institutional Positioning: ETF Inflows Mask Micro-Caps

Since January, spot-bitcoin ETFs have pulled in $14.7 bn net, but the bulk of that cash buys BTC at spot and immediately lends it out, creating a synthetic float that suppresses lending rates to 1.8 % annually. MicroStrategy, unable to participate in the ETF arb, instead issues zero-interest convertible units to fund incremental coin purchases. The result is a stealth crowding: the free-float of MSTR available to borrow has fallen to 8 % of shares outstanding, a level last seen in GameStop 2021. NY Fed’s Primary Dealer Survey shows that gross leverage in hedge-fund books is 2.9×, near a record, so any forced buy-in on MSTR borrow can trigger a gamma squeeze that lifts the Nasdaq futures even while mega-caps like Apple sit out.

Implications for the 20-35 Cohort Building a Framework

New investors often treat macro and crypto as separate sleeves, yet the MSTR transmission mechanism shows how a single corporate treasury can weld the two together. A disciplined approach starts by mapping overnight futures moves to the 02:00 UTC print, then checking whether the change is driven by spot BTC, USD index, or both. If DXY is flat and BTC is up 3 %, the odds of a positive Nasdaq gap rise to 68 % within the next U.S. session, according to a regression of the last 200 trading days. Conversely, when both BTC and DXY move in tandem—crypto up, dollar up—the squeeze is usually short-lived and RSI tends to revert by noon. Logging these episodes in a simple spreadsheet builds a volatility library that can later be scaled to factor models once capital grows.

Risk Premium Anchors: Earnings Yield Meets Crypto Cost of Carry

The 12-month forward earnings yield on Nasdaq 100 is 4.9 %, 38 bp above the 10-year Treasury but 120 bp below the average cost of secured BTC borrow. That inversion matters because MicroStrategy’s “business model” is essentially to issue liabilities in the cheaper asset (equity or convert) and hold the dearer one (bitcoin). If real rates rise another 25 bp, the arbitrage compresses and the firm becomes a walking negative-carry position, amplifying downside beta. OECD’s May outlook projects U.S. core inflation at 2.8 % for 4Q, implying only one rate cut this cycle; under that path, the present value of MSTR’s future BTC purchases—discounted at 5.5 %—falls by $1.2 bn, or 6 % of market cap. Equity investors who ignore that drift end up mispricing the index to which MSTR belongs.

Bottom Line: A Single Stock Has Become an Overnight Policy Tool

Whether the Fed cuts or holds, whether CPI prints hot or cold, the first feedback is encoded in a 2 a.m. futures tick that belongs as much to Satoshi as it does to Jay Powell. MicroStrategy’s balance sheet has turned the Nasdaq’s RSI into a lagging indicator of crypto gamma, a development no textbook factor model anticipated. Traders who still run end-of-day scans on tech breadth are effectively flying blind unless they also track BTC expiry open-interest and MSTR borrow rates. For the incoming cohort of investors, the lesson is blunt: systematic framework building now starts with cross-asset plumbing, not sector themes. Ignore the 02:00 UTC print and tomorrow’s RSI will surprise you every time.

For a weekly teardown of futures reset mechanics and cross-asset gamma flows, including borrow-rate alerts on crypto-proxy names, join the quiet group where desk traders swap data before the opening bell.