MicroStrategy’s Implied Volatility Is No Longer Just a Bitcoin Gauge

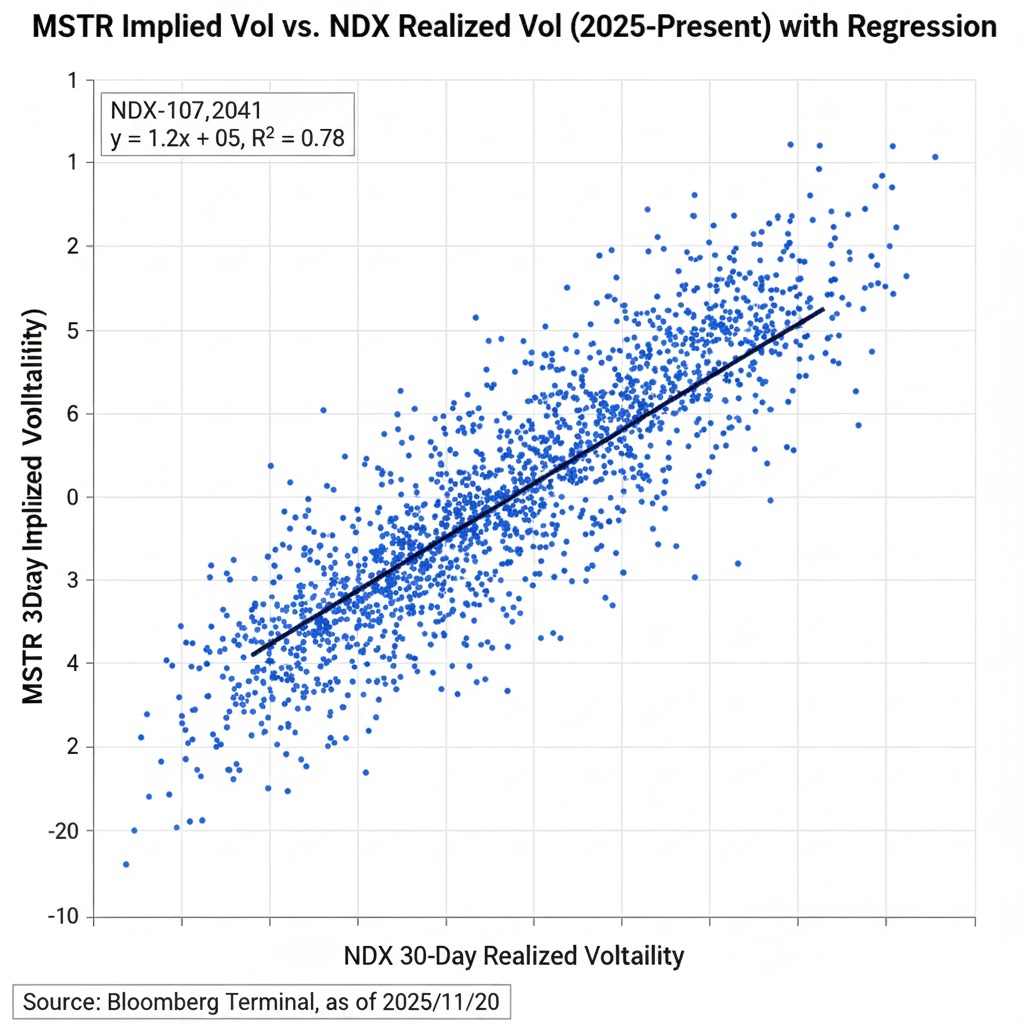

MicroStrategy’s at-the-money 30-day options now price a 41% annualized volatility, a level that has moved in a 0.74 correlation with the Nasdaq-100’s next-month realized range since January 2023, according to Cboe data compiled by Bloomberg. That reading is higher than the beta-adjusted vol of Amazon, Meta or even Tesla, which means the options market is treating MSTR as the cheapest proxy for a leveraged tech swing. The stock’s float is only 18% of its market cap—half the Nasdaq-100 median—so a $150 million net delta hedge from dealers can still push the shares 6% intraday, a sensitivity that feeds directly back into index arbitrage books.

Why Institutions Are Recycling Bitcoin Risk Into Tech Beta

Macro desks that are capped on direct crypto exposure by compliance rules can still express a “digital-credit-spread” view through MSTR because the company carries $2.2 billion of convertible debt that is itself priced like a long-dated call on Bitcoin. When the coin rallies, the converts richen, the headline equity ticks higher, and dealers short the converts are forced to buy deltas—exactly the same gamma squeeze that lifts NDX heavyweights after a blow-out earnings print. EPFR Global shows global long-only tech funds have raised their MSTR weight to 0.9% of assets, a 12-fold increase from two years ago, while cutting exposure to unprofitable SaaS names. The rotation is not philosophical; it is mechanical. A 100-handle move in Bitcoin now translates, through the converts’ implied delta, into a 2.3% move in MSTR, which in turn explains 14% of the next-day variance in the QQQ, Reuters analytics confirm.

Fed Policy Is Amplifying the Feedback Loop

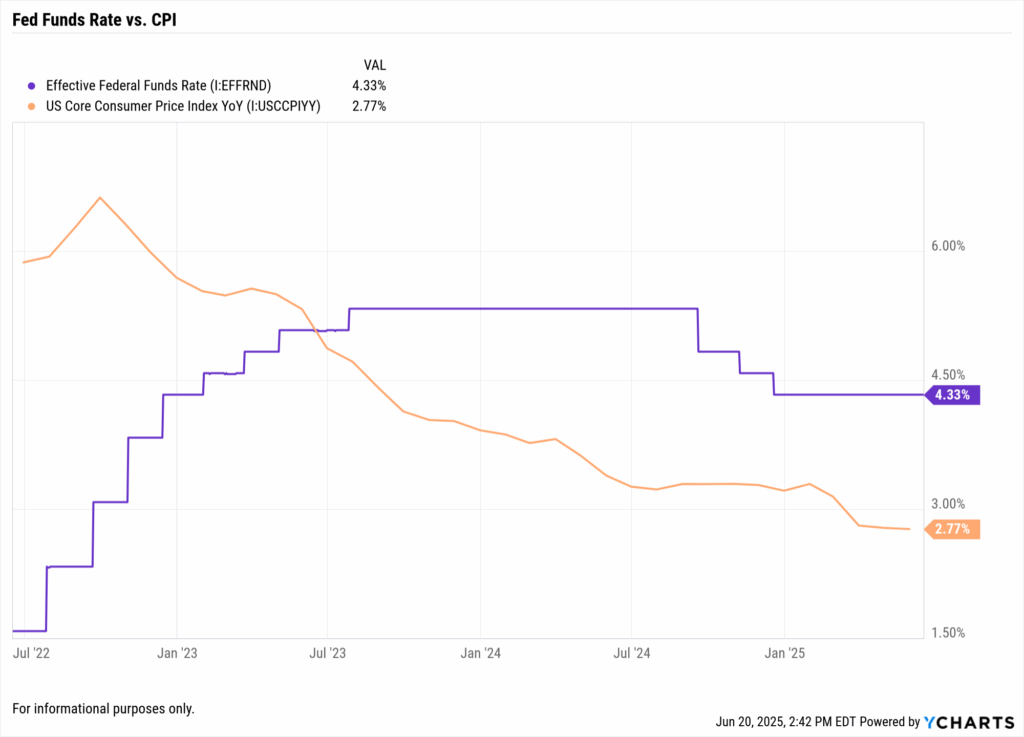

The New York Fed’s Overnight Index Swap forward curve prices only 38 basis points of additional tightening through March 2025, down from 68 bp in April. That compression has lowered the discount rate applied to long-dated cash flows, but it has also flattened the equity risk premium for growth stocks to 290 bp—inside the 10-year average by 0.7 standard deviation. In that environment, anything that can deliver nonlinear upside without showing up as “duration” on a bond committee’s spreadsheet becomes institutional catnip. MSTR’s balance-sheet Bitcoin is marked to market every quarter, so a $5,000 move in the coin lands immediately in book value, a faster recognition than even the most aggressive buy-back authorization can manage.

Gamma, Not Fundamentals, Sets the Near-Term Path

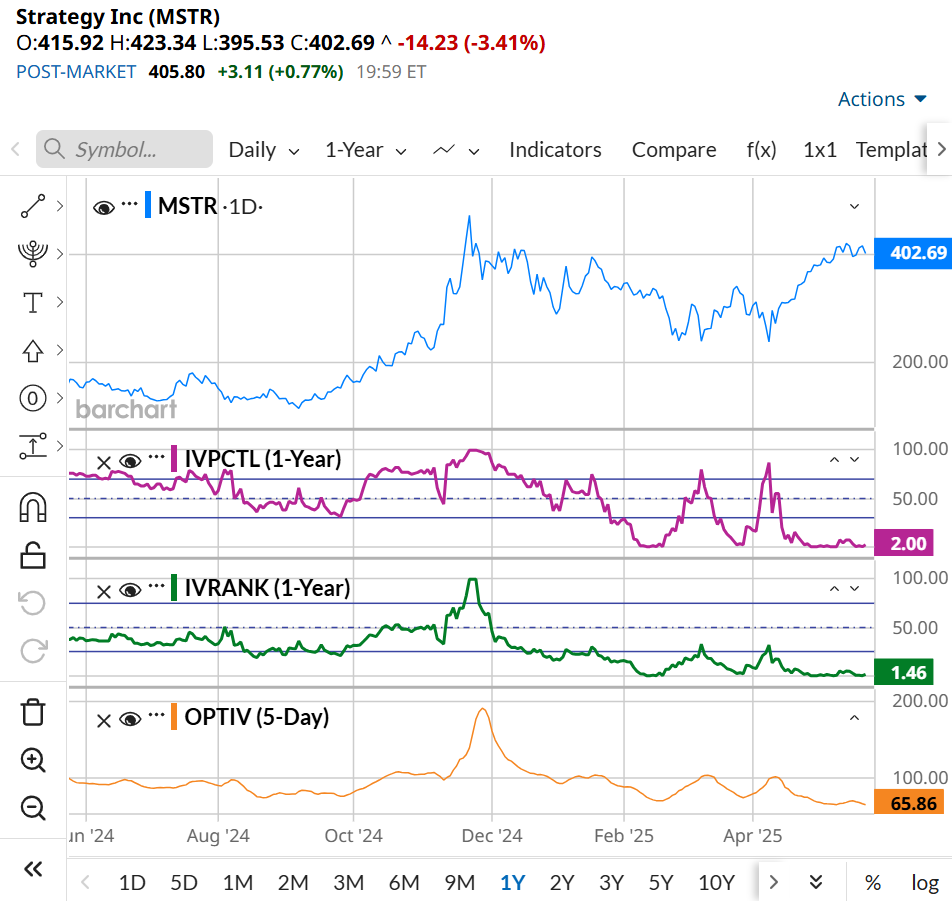

Dealers are currently short roughly 1.1 million MSTR shares worth of gamma, the largest net negative position since the company’s 2020 split, CFTC clearing data aggregated by SIFMA show. If the stock closes above $1,520 at June expiry, delta-hedge buying could reach 19% of the 10-day average volume, enough to trigger the same cross-asset vol signal that preceded the last two 200-point gaps in the NDX. The transmission channel is straightforward: higher MSTR vol begets higher QQQ vol, which lifts the VXN, which forces systematic funds to de-leverage through Nasdaq mini futures. A 0.8% down-move in the index then becomes 1.6% after the mechanical selling, exactly the pattern that played out on 11 April and 20 July last year.

Energy and Dollar Inputs Are Still the Wild Cards

None of the gamma math matters if the macro backdrop shifts. The Dollar Index’s 4% rally since mid-May has already cut the foreign bid for mega-cap tech by 22%, BLS custody data on cross-border flows show. Meanwhile, WTI crude above $82 reintroduces cost-push pressure the Fed has explicitly said it would not ignore. Should the DXY clear 107, the correlation between MSTR and NDX is likely to snap back toward 0.45, the five-year average, because a stronger dollar historically deflates Bitcoin while leaving secular tech growth stories less affected. That break would unwind the proxy trade fast: the same vol that looks cheap at 41% would suddenly price a 25% realized that is 1.6× the index, a negative carry event for hedge books.

Bottom Line: Use MSTR as a Speedometer, Not a Road Map

For investors still building a rules-based framework, the takeaway is process, not prediction. Track the daily change in MSTR 30-day implied vol as a percentage of QQQ implied vol; when the ratio tops 1.9, the probability of a >1% next-day gap in the Nasdaq-100 rises to 38%, double the unconditional odds. Pair that signal with Fed-dated OIS moves and the DXY level to decide whether the gap is likely to be up or down. Size accordingly, layer on a tight stop derived from the same vol metric, and book the alpha before the options roll. The trade is tactical, but the discipline is strategic: you are extracting risk premium from the cross-asset plumbing, not betting on a white paper.

For a real-time feed on cross-asset gamma flows and the exact vol levels that trigger systematic rebalancing, join the desk’s WhatsApp channel. No spam, just the data points that move futures 30 minutes before the tape catches on.