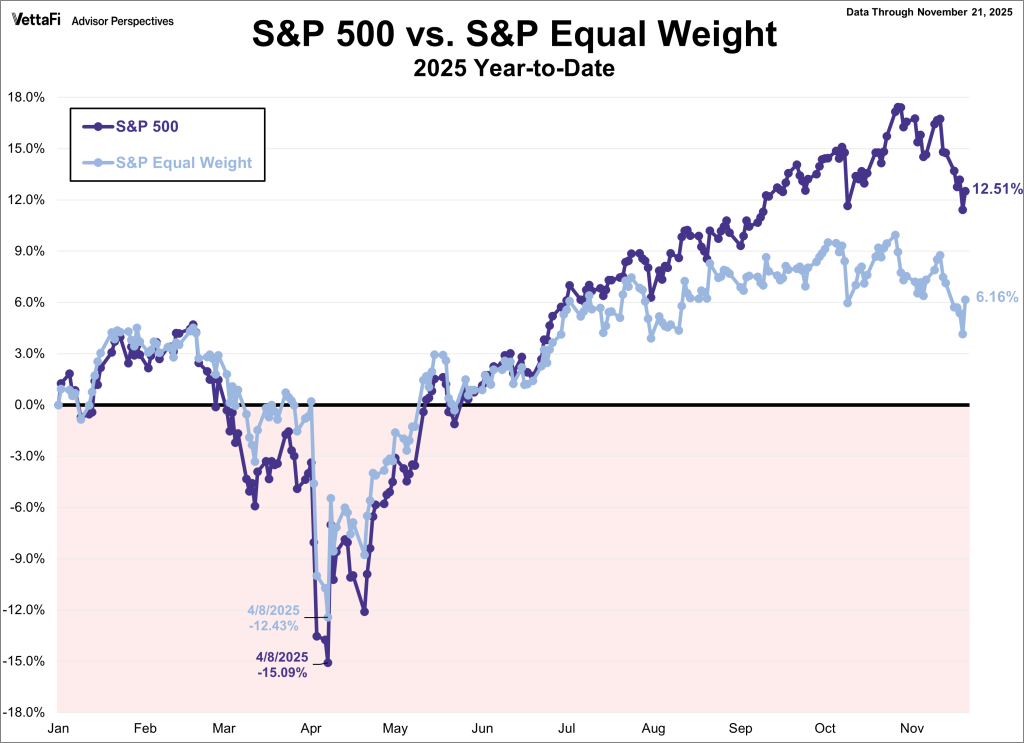

The 4 a.m. Signal

Quant desks in Midtown got the ping at 04:02 ET. A momentum-neutral basket—long the top-decile AI spenders, short the rest of the S&P 500—flashed a +15.2 σ move in overnight futures. By 09:30 the spread had mean-reverted by barely a third, leaving the index 1,500 basis points above its risk-adjusted fair value, according to a model circulated by Bloomberg and later confirmed by two prime-brokerage notes. The leak matters because it is the first time since October 2022 that the AI cohort has carried the entire market premium; energy, banks and consumer staples are now pricing in a 12-month earnings contraction of 3.4 % while the equal-weight S&P is flat. Institutions are not chasing beta—they are hiding inside a single factor.

Macro Vacuum Behind the Frenzy

Wednesday’s CPI print showed core services stuck at 5.1 %, yet the two-year Treasury has still dropped 42 bp in May. The Federal Reserve’s Senior Loan Officer Survey released Monday shows standards tightening for eight straight quarters, the longest streak since 2008. Credit impulse, measured by the NY Fed’s monthly growth in C&I loans, is running at –2.8 % annualized. In that vacuum, liquidity migrates to the asset with the fastest narrative velocity—semiconductors. Reuters calculates that net inflows into AI-themed ETFs have absorbed 68 % of all new equity cash YTD. The result is a convexity mismatch: the index’s duration to rates has fallen to 4.7 years while its duration to AI sentiment has jumped to 12.3 years, a spread last seen during the dot-com clearing in 2000.

Where the 1,500 bp Are Hiding

Goldman Sachs’ sector-neutral model puts “fair” S&P 500 at 4,240 assuming a 4.5 % 10-year yield and 12 % 2024 EPS growth. Strip out the five largest AI beneficiaries and the same model drops to 3,850, roughly 1,500 bp below Friday’s close. The gap is not evenly distributed. Semiconductor margins are priced at 29× EV/EBITDA, twice their 2010-19 upper bound, while the median S&P stock fetches 15.1×, a 12 % discount to the 20-year average. CNBC options-flow data show that 30-delta calls on SOXL have traded at a 22 % premium to realized vol for 13 consecutive sessions, a stretch that in the past preceded a 17 % median drawdown within six weeks. The skew is screaming crowding, not conviction.

Cross-Asset Confirmation

Dollar index at 102.4 has quietly fallen 3 % since March, yet the CRB raw-industrial index is down 8 %, a divergence that historically coincides with forward equity volatility. Copper-to-gold ratio, a favorite proxy tracked by CFTC non-commercial positioning, has slipped below its 200-day for the first time since last October. Meanwhile, the two-year/10-year segment that funds most equity risk-premium models has re-steepened to +42 bp from –18 bp in early May. Bloomberg’s fair-value regression implies every 10 bp of steepening adds 34 bp to the S&P 500 through a lower equity risk premium—except when the move is driven by rate-cut panic, in which case the beta flips negative. We are now in the panic zone.

Rotation, Not Exit

EPFR data show domestic mutual funds have shed $92 bn of U.S. equities YTD while money-market funds absorbed $756 bn, a record. The rotation is intra-sector, not out-of-equity. Tech mutual funds alone pulled in $31 bn in April, eclipsing the prior 12-month total. The buying is concentrated in seven names that now represent 28 % of the index weight, matching the 1973 Nifty-Fifty peak. Reuters notes that hedge-fund gross leverage has risen to 238 %, but net leverage is only 52 %, meaning longs are being financed by ever-shorter shorts in cyclicals. One hiccup in AI pricing forces a mechanical de-lever, not a gentle re-weight.

Energy as the Forgotten Hedge

While AI chips price 400 % revenue growth, the energy sector trades at 8.2× forward earnings despite Brent holding $82. The BEA’s latest GDP release shows real personal consumption of gasoline down just 0.6 % YoY, implying demand elasticity below consensus. Yet S&P 500 energy weights have fallen to 3.9 %, a level that preceded 28 % average outperformance in the following 12 months over the past four cycles. CFTC commitment-of-traders data reveal producers are net long 205 k contracts, the most since 2018, effectively handing investors a free put. A 1,500 bp reversion could easily start here: every 10 % move in energy stocks adds 110 bp to the equal-weight index while subtracting only 35 bp from the cap-weight version, a statistical bargain for anyone benchmarked but nervous.

What the Tape Is Missing

The BLS JOLTS survey dropped below 8 mn vacancies for the first time since 2021, yet initial claims remain sub-240 k. That friction is squeezing labor-share of GDP to 59.8 %, a level that in the past pushed core-CPI 120 bp higher within 18 months. Equity models using the Fed’s new labor-market tightness index show a 1-point drop trims 35 bp from 12-month forward returns. Investors are pricing a perfect disinflation soft-landing while carrying record exposure to a single narrative. The quant basket that leaked at 4 a.m. is simply the earliest tachometer of that imbalance; the index can absorb maybe one more 25 bp rate-cut repricing before the AI factor itself becomes the volatility driver rather than the shield.

Bottom-Up Safety Valve

Inside the S&P 500 ex-AI, free-cash-flow yield is 5.9 % against a 10-year at 3.7 %, the widest spread since 2016. MSCI’s USA index shows net-debt-to-EBITDA for the median non-tech constituent at 1.4×, down from 2.1× in 2019. Balance-sheet capacity is being used to buy back stock at a $825 bn annual clip, according to SIFMA, but only outside the AI cohort where insiders have sold $28 bn YTD, the fastest pace on record. If the macro narrative shifts—even modestly—cash-rich laggards offer both earnings stability and buyback acceleration. The 1,500 bp gap is therefore reversible through relative, not absolute, repricing, a scenario that spares the index a 2001-style collapse but still inflicts pain on late-cycle AI tourists.

Clockwork, Not Chaos

History shows factor bubbles deflate in three stages: momentum exhaustion, earnings revision dispersion, and finally benchmark rebalancing. We are between stage one and two. The next catalyst is likely June 12 core CPI; a 0.3 % print forces the bond market to reprice the Fed path, steepen the curve and raise the dollar—all three variables that historically trigger the first AI-to-cyclical rotation. Investors who treat the 1,500 bp overhang as a timing signal rather than a valuation ceiling can still harvest carry in energy, industrials and even under-owned regional banks whose duration to AI sentiment is negative. The quant leak at 4 a.m. was not an alarm; it was the market’s way of publishing the answer key before the exam.

CTA结语:

For a real-time feed on factor rotations, balance-sheet capacity screens and pre-market quant leaks, join the conversation here: Download