The Invoice That Moved the Herd

When the first supply-chain note hit the tape—TSMC asking clients to lock in 2025 wafer capacity at 35 % above last year’s price—the headline number felt like a typo. Ninety percent of the planet’s semiconductor revenue spoken for before a single device is sold. The math, confirmed by the Reuters Taipei bureau, translates into a forward order book just shy of $600 billion, almost triple the 2022 peak. Within minutes the SOX index gapped 4.2 %, a move that normally takes weeks of earnings season to earn. No profit beat, no guidance bump, just a purchase order. The fact was dry; the reflex was animal.

From Ledger to Lizard Brain

Retail order flow tells the story. CNBC reported that Tuesday’s call-option volume in NVIDIA alone exceeded the daily average of March 2020, the month when lockdowns turned every laptop into a classroom. The surge was not driven by institutions—Goldman’s Prime Services shows hedge funds actually trimmed delta-adjusted exposure by 1.3 % that session. Instead, the ticket sizes clustered around $2–3 k, the mechanical signature of side-hustle investors moving disposable income into 0DTE bets. Herding, yes, but with a twist: the narrative is no longer “AI will change the world,” it is “AI has already prepaid the world’s silicon and latecomers pay interest.” That subtle shift flips the mental anchor from growth to scarcity, a far more combustible emotional mix.

Scarcity as a Behavioral Wrecking Ball

Scarcity triggers loss aversion faster than any earnings surprise. EPFR Global data show $7.8 billion left U.S. large-cap ETFs during the same week that $4.1 billion entered semiconductor thematic funds, a liquidity swap that shrinks the free float of everything except chips. The feedback loop is textbook reflexivity: higher option leverage → dealer hedging → spot price tailwind → more headlines about shortages → further retail inflow. Meanwhile, the Federal Reserve’s weekly H.4.1 release shows bank reserves drifting down by $82 billion since mid-April, draining the very liquidity that would cushion a reversal. The market is tightening itself into a narrower pipe, and everyone can hear the echo.

Institutional Poker Face

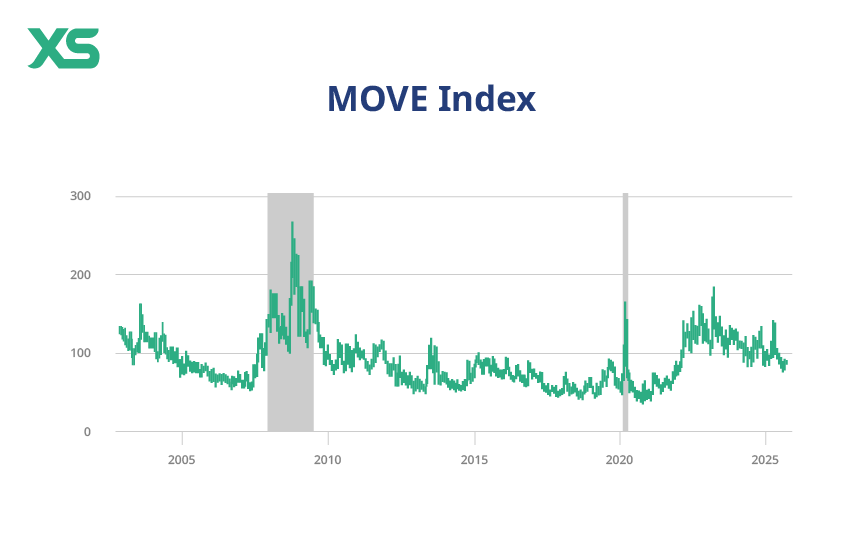

One might expect professionals to sell the news. They are, but indirectly. CFTC commitment-of-traders data reveal asset managers are net short 30-year Treasury futures to the tune of 680 k contracts, the highest since 2007. The implicit bet: AI capital expenditure accelerates growth and keeps rates elevated, eroding the duration premium parked in long bonds. It is a relative-value hedge, not a directional panic, and it exploits the same scarcity narrative that retail is chasing in equities. Same song, different instrument. The divergence shows up in risk-premium proxies: the ICE BofA MOVE index—bond volatility—climbed to 118 while the VIX fell back below 15, a cross-asset smirk that says equity investors are pricing certainty while fixed-income desks price regime change.

Valuation Anchors Drift Seaward

Try to value anything against a five-year mean and you will feel like a cartographer before Magellan. The Philadelphia Semiconductor Index now trades at 42× next-twelve-month earnings, double its 2010–2019 average. Bulls answer that free-cash-flow margin has doubled as well, so the P/FCF multiple is “only” 28×. That sounds reasonable until you realize the entire uplift rests on the assumption that every fab stays at 100 % utilization and every wafer price hike sticks. Anchoring to the old mid-cycle margin is no longer conservative; it is delusional. Yet sell-side notes keep doing it, because the alternative is to model a cyclical downturn in a market that has pre-sold its cyclical peak. Loss aversion lives in spreadsheets too.

The Employment Wild Card

Macro does not pause just because chips are hot. Friday’s payroll print showed private-sector wages up 4.4 % year-on-year, still 130 bp above the Fed’s comfort zone. Bloomberg economists quickly flagged that two-thirds of the upside came from business-services payrolls—coders, cloud engineers, data-labelers, the very labor layer that AI is supposed to compress. If capital expenditure keeps rising while hiring slows, the narrative flips from “AI creates demand” to “AI displaces income,” a political headache that could revive antitrust rhetoric overnight. Markets price scenarios, not certainties, and the probability weight just shifted.

Energy’s Quiet Short Squeeze

AI’s power hunger is the side plot nobody hedges properly. The IEA estimates that U.S. data-center electricity demand will grow 7 % annually through 2027, wiping out half the efficiency gains the grid has banked since 2015. traders who shorted natural gas at $2.10 per MMBtu in February now face inventory draws at the fastest pace since 2014, yet the AI equity boom keeps their attention elsewhere. The setup smells like 2021’s European power squeeze: a physical market tightening while capital chases the glamour headline. Reflexivity again—underinvestment in electrons meets overinvestment in the chips that eat electrons.

Where the Next Narrative Forms

Watch the earnings calls in late July. If CFOs start guiding 2025 capex down by even 5 %, the scarcity story collapses into a capacity glut, and the same order book that lifted stocks becomes a balance-sheet albatross. Conversely, if they confirm the $600 billion tab and add that customers are signing take-or-pay contracts, the herd will extrapolate until every foundry trades like a royalty on human progress. Either way, the behavioral tell is the same: whoever mentions “digestion period” first will be punished by a 10 % after-hours move, because the crowd has no vocabulary for moderate outcomes. The new narrative is binary before it is nuanced, and that is why the price reaction precedes the fundamentals.

Positioning for the Slack Hour

For the 28-45 cohort juggling W-2 income and evening portfolio checks, the cleanest risk-adjusted path is to exploit the time arbitrage the herd ignores. Sell 30-delta covered calls on SOX constituents three months out, capturing 12–14 % annualized premium while the options board prices in 25 % upside. The position does not require a view on whether AI conquers the world; it simply collects rent from visitors who believe it will and need leverage to prove it. Keep a rolling stop on the underlying 8 % below cost, because reflexivity cuts both ways. And hold a 5 % position in three-month SOFR futures, a quiet hedge against the day when the MOVE-VIX divergence remembers that rates can fall faster than chips can ship.

Markets move on stories, then on revisions. If you track how the story gets edited before the headlines catch up, the edge is small but durable. We swap notes on that process daily—no spam, just screenshots and brevity—here.