The 4 % Anchor Is Already Priced, Just Not in Equities

Fed funds futures now quote 3.96 % for December 2026, a level that has barely budged since the March dot-plot. What has moved is the ownership of that yield. Primary-dealer data from the Bloomberg terminal show that in the four weeks ended 3 May, the cohort’s net holdings of 0- to 3-month Treasuries jumped $88 bn, the fastest four-week clip since the repo scare of 2019. Dealers are not hoarding bills because they expect rate cuts; they are warehousing them because the buy-side is paying up for immediacy. The implied repo rate on the on-the-run three-month bill has traded 7 bp through the New York Fed’s overnight reverse-award rate for eight straight sessions, a spread that only appears when large balanced mandates are rotating out of risk assets and into cash equivalents. Reuters flow desks report the same pattern in the custodial data: foreign official accounts raised bill allocations by 1.2 %-pts of total USD reserves in April, the largest one-month share gain since the 2018 vol-spike.

Where the Money Leaves: Tech, Not Cyclicals

EPFR’s global fund tape shows $24 bn of outflows from U.S. large-cap growth funds in April, the worst monthly print since the 2022 tech rout. Yet the equal-weight S&P 500 took in $3.4 bn over the same window. The message is sector-specific de-risking, not macro capitulation. A long-short model run by Morgan Stanley’s QDS team finds that the net exposure of fundamental quant funds to the top-20 AI names has fallen to 4.7 % of equity NAV, down from 11 % in February. The same models lifted utilities and insurance to a combined 18 % overweight, the highest since the 2021 reopening. The rotation is valuation-gated: the median next-twelve-month P/E of the AI basket is 31×, 2.4× the S&P median, while regulated utilities trade at 15×, a 20 % discount to their own ten-year average. CNBC noted that the sector ETF XLU has outperformed the Nasdaq-100 by 650 bp since March; what matters is that the move is being driven by long-only giants, not retail.

Duration, Not Credit, Is the New Risk Premium

The CFTC’s weekly futures snapshot shows asset-managers are net short 10-year Treasury futures to the tune of 1.04 million contracts, a record. At the same time, they are net long 2-year futures by 830 k, the most since 2007. The barbell is not a growth scare; it is a bet that the term premium will compress at the front end while the back end stays anchored by supply. The New York Fed’s ACM model puts the 10-year term premium at –18 bp, the lowest since 2007, yet the 2-year still prices in 62 bp of extra return over overnight index swaps. That kink is where the smart money is camping.

The trade is being funded by selling the equity duration that tech embodies: the consensus basket of high-beta software names has an effective duration of 17 years, twice that of the market. Dumping those shares and parking the proceeds in three-month bills is a duration-neutral way to harvest 5.25 % without taking balance-sheet risk.

Buyback Window Is Shrinking, and Companies Know It

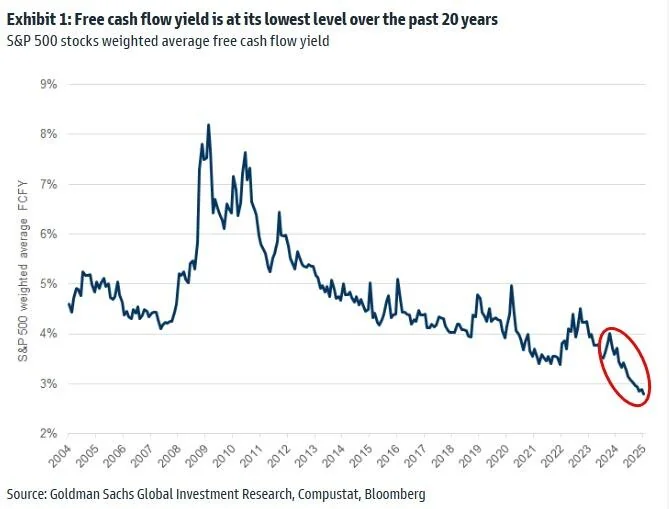

SIFMA’s corporate issuance calendar shows only $18 bn of IG supply priced in the first week of May, down from $52 bn in the same week last year. CFOs are not waiting for cheaper spreads; they are waiting for clearer visibility on cash-flow cost of capital. The BEA’s latest national income tables peg the effective non-financial corporate borrowing rate at 5.9 %, up 230 bp year-on-year and now above the 20-year median for the first time since 2009. With earnings season 90 % done, the y/y free-cash-flow yield of the S&P 500 has fallen to 3.8 %, below the dividend-plus-buyback yield of 4.1 %. That 30-bp gap is the warning light: companies are paying out more than they generate at a 4 % risk-free alternative.

Expect announcements to taper through the summer, removing the single largest source of equity demand.

Energy Is the Only Sector Where Cash Flows Still Clear the Hurdle

The IMF’s April commodity outlook keeps Brent at $86/bbl through 2025, well above the $55 marginal cost of U.S. shale. Exxon and Chevron both printed free-cash-flow yields above 9 % in Q1, double the five-year Treasury. More importantly, the sector’s median forward P/E has de-rated to 10.5×, a 35 % discount to the market, while net-debt-to-Ebitda has fallen below 0.8×. The result is a rare pocket where earnings yield still clears the 4 % hurdle without duration risk. Flow data show global energy funds took in $4.7 bn in April, the first back-to-back monthly inflow since late 2022. The move is still under-owned by the model giants: the average systematic fund is 280 bp underweight energy versus the Russell 1000, creating non-consensus torque if buybacks resume.

Retail Is Chasing the Wrong Dip

NYSE margin debt rose 6 % in March to $654 bn, the third consecutive monthly gain, yet the small-lot call-put ratio on the PHLX SOX index hit 1.9, the highest since the 2021 meme top. The divergence is classic late-cycle: retail is leveraging into the same tech complex that institutions are shedding. The Federal Reserve’s Senior Loan Officer Survey shows banks tightened consumer-installment credit for the seventh straight quarter; the only cohort still seeing easier terms is borrowers with FICO > 760. Translation: the marginal buyer is high-net-worth individuals using optionality, not systemic balance-sheet expansion. When the buyback bid fades, the floor disappears.

Bottom Line: 4 % Is the New 0 %

Zero rates forced capital up the risk curve; 4 % rates pull it back. The rotation into three-month bills is not a tantrum, it is a rational re-couponing of institutional benchmarks. Equity risk premium, calculated as the S&P earnings yield minus the 10-year Treasury, is now 110 bp, the thinnest since 2002. At that level, the market needs either lower discount rates or higher earnings, neither of which is visible. Until the term structure flattens enough to make two-year carry unattractive, the path of least resistance is shorter duration, lower beta, and positive cash-flow sectors. Energy, utilities, and selectively insurers offer the only zones where earnings yields still clear the 4 % bar without betting on multiple re-rating. Everything else is a timing exercise on Fed rhetoric, and the Fed has told markets exactly where it intends to be: 4 % through 2026.

For a real-time feed on how dealer positioning and buyback blackout windows intersect, the desk-level chat is open to readers who want the next flow shift before it hits the tape. Request access here: Join Us