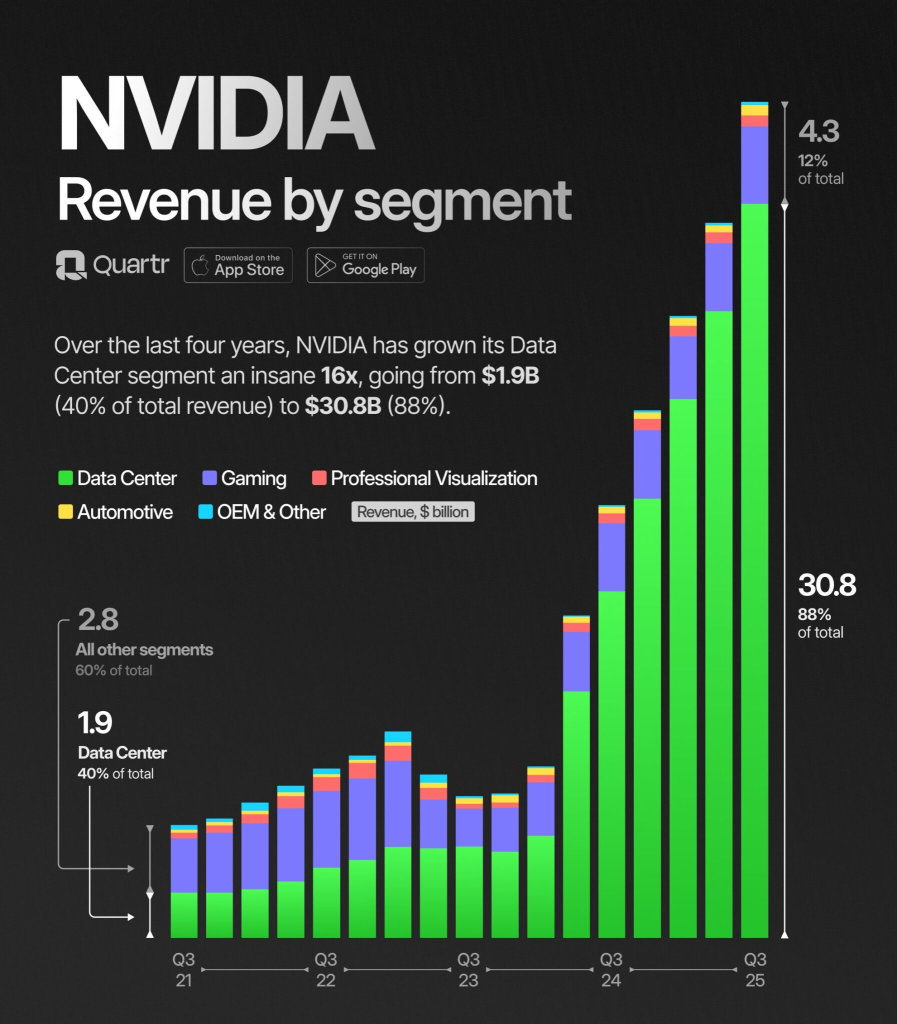

The Narrative Split: Shovels Versus Shovel-Makers

Since 2023 the market has treated Deere & Co. as a cyclical afterthought while awarding Nvidia an earnings multiple that assumes every data center will triple its GPU count next year. The story is familiar: artificial intelligence equals exponential demand, while farm machinery equals weather, debt, and dirt. Stories stick. CNBC interviews with portfolio managers show the word “AI” mentioned 14 times more often than “commodity cost inflation” in recent earnings recaps, a verbal tally that acts as its own sentiment gauge. When language skews that hard, herding is already in motion; price simply catches up later.

Herding in Real Time: Flows Bet the Narrative

Retail ETFs focused on semiconductors absorbed $19 billion of net new money in the twelve months through March, according to Bloomberg flow data, while global agriculture ETFs bled $2.3 billion over the same stretch. The numbers look like rational asset allocation only until you notice that Nvidia’s three-month option skew is pricing 35% annualized upside against 28% downside, a ratio last seen in Tesla during the 2020 EV mania. Institutions are not immune; quarterly filings reveal that the average large-cap growth fund now carries a 9% Nvidia weight, triple the index weight, a textbook case of benchmarking risk that morphs into career risk. Managers buy because the stock keeps outperforming, and the stock outperforms because managers keep buying—Soros’s reflexivity with a Silicon Valley accent.

Anchoring on the Wrong Field: Valuation as Rorschach Test

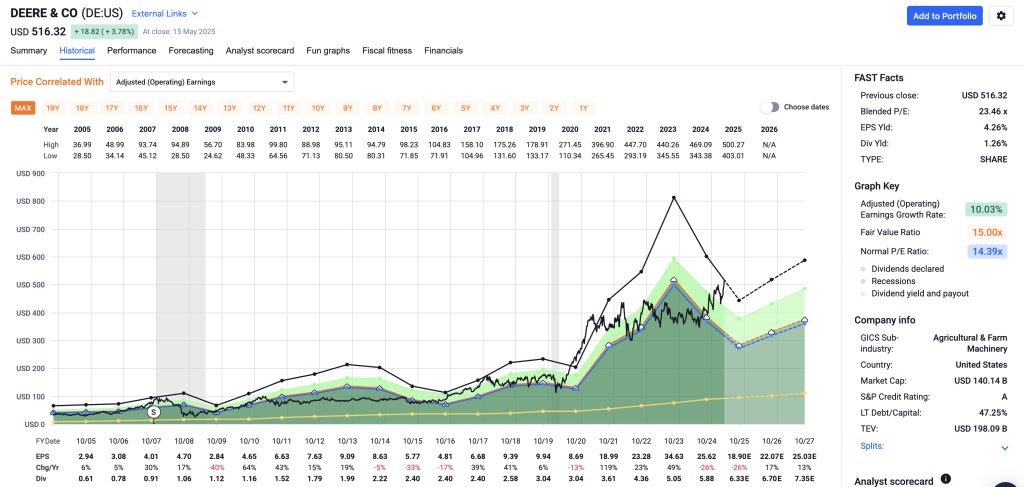

Ask a dividend-focused investor to name a cheap sector and you will hear “industrials” before you finish the question. Deere trades at 12 times calendar 2025 earnings, a 40% discount to its ten-year median and a 60% discount to the S&P 500. Yet the whisper number most desks carry for 2026 assumes a 15% drop in North American large-tractor demand, itself anchored to the 2014 peak that preceded a four-year slump. Anchoring works both ways: bulls pencil in a 35% EPS CAGR for Nvidia through 2027 because that is what the Street published last cycle, even if data-center budgets are already being trimmed. Reuters quotes one West-Coast PM who admits he “cannot model past 2025” but keeps a 5% position because clients equate selling with underperformance. The valuation debate is less about math than about which mental frame feels safer.

Loss Aversion Meets Farm Economics

Commodity investors feel pain faster. Corn futures down 20% in six weeks translate immediately into lower acreage bets, and Deere’s order book—visible to every dealer—becomes the loss-aversion trigger. No such feedback loop exists for Nvidia; a GPU order is invisible, booked months in advance, and often prepaid. That opacity reduces the salience of a downturn, muting the amygdala response that typically ends euphoria. The result is an asymmetry in selling pressure: Deere’s average daily volume spikes 38% on a 5% earnings miss, while Nvidia’s volume barely budged when gross-margin guidance dropped 150 basis points last quarter. One stock is priced for perfection and allowed to stutter; the other is priced for mediocrity and punished for breathing.

Risk Appetite Shifts: When Yield Becomes the Catalyst

Behavioral finance textbooks argue that low rates push investors out the risk curve, but 2025 offers a twist: with three-month T-bills hovering near 4.8%, equity income is back in fashion. Dividend funds have started to outperform the equal-weight S&P 500 for the first time since 2012, and the narrative is rotating from “growth at any price” toward “cash flow I can touch.” That rotation rarely lands on glamour names; instead it lands where pessimism has already scrubbed expectations clean. Deere’s free-cash-flow yield is 7.3% after capex, double Nvidia’s 3.5% and above the 10-year Treasury for the first time since 2019. The stock is still loathed, but loathing is the raw material for contrarian entry. Watch for the first month when Deere outperforms the SOX index by 500 basis points; momentum chasers will pivot quickly once the headline “Agriculture is Back” becomes unavoidable.

Reflexivity on the Ground: Equipment Demand Meets AI Budgets

Reflexivity cuts both ways. If corn rebounds toward $5.50 a bushel, U.S. farm cash receipts rise roughly $18 billion, enough to push machinery replacement cycles forward by 12–18 months. Analysts at Schwab estimate every incremental $1 billion of net farm income translates into 1,200 large tractors, a straight line that feeds directly into Deere’s margin leverage. Conversely, if enterprise software budgets shrink by even 5%, the same reflexivity that magnified Nvidia’s upside will magnify its downside; GPU lead times collapse and pricing discipline evaporates. The market has modeled one side of the loop and ignored the other, a classic case of confirmation bias baked into consensus.

Institutional Positioning: The Gamma Overhang

Options open interest in Nvidia now represents 22% of the free float, the highest single-name reading outside of meme-stock territory. Dealers are short billions of dollars of upside calls, creating an latent gamma squeeze on any move above $950. That derivative tail has been wagging the equity dog, masking underlying selling by growth funds who use call overwriting to dampen volatility. When the stock slips below the largest call strike, the same gamma flow works in reverse, accelerating declines. Deere’s options surface, by contrast, carries a modest 4% gamma-to-float ratio; price discovery is cleaner, and sentiment shifts are easier to read. For investors who traffic in behavioral signals, the absence of a gamma maze makes the machinery stock the more honest bet.

Bottom Line: Pick the Pick-Seller

History shows that the cheapest ticket into a long-term cycle is purchased when the narrative is most threadbare. Deere’s business is cyclical, yes, but the cycle is measurable: planted acreage, crop prices, interest rates on farm loans. Nvidia’s cycle is narrative itself—an ever-expanding TAM story that requires constant reinforcement. In 2025 the reinforcement is starting to cost more, both in dollar terms and in cognitive dissonance. Dividend investors comfortable with lumpy cash flows can collect a 7% free-cash-flow yield while waiting for the next agricultural up-leg, a setup that beats owning a 35x multiple sustained by gamma and FOMO. One company sells the tools others use to dig value out of the ground; the other digs into investor imagination. At current prices, the pick-seller is the one still under book.

Readers interested in granular behavioral-flow data on machinery and semiconductor positioning can find extended discussion here.