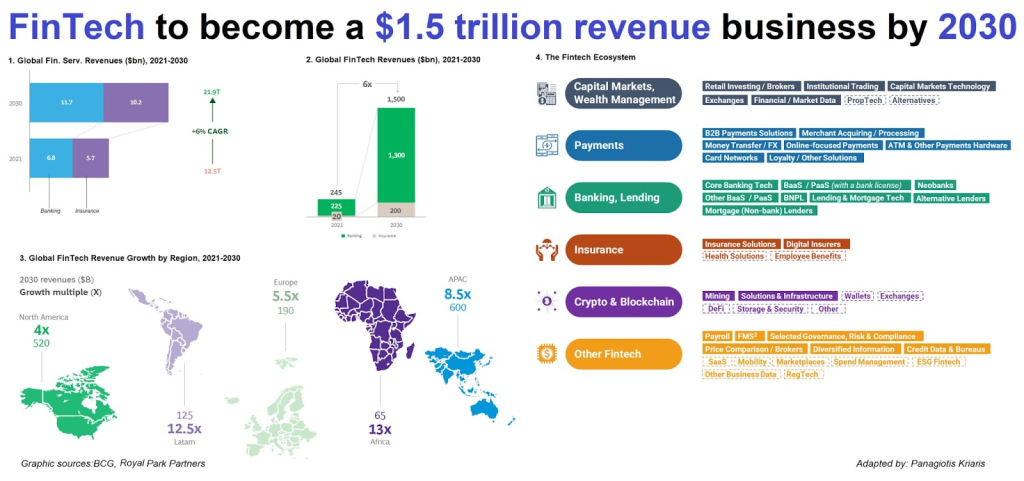

The digital banking landscape is undergoing a seismic shift, driven by advancements in financial technology (FinTech) that are reshaping how consumers and businesses interact with their finances. As we stand on the brink of a $1 trillion revolution, it is essential to understand the implications for investors navigating the U.S. stock market. The convergence of traditional banking and innovative FinTech solutions presents both challenges and opportunities that could redefine investment strategies.

The Current State of Digital Banking

According to recent reports from Bloomberg, digital banking assets have surged as consumers increasingly favor online platforms over brick-and-mortar institutions. This trend has been accelerated by the pandemic, which forced many to adapt to remote services. In 2023, global digital banking revenues are projected to exceed $500 billion, with significant contributions from mobile payment solutions and peer-to-peer lending platforms.

As interest rates remain historically low, traditional banks are struggling to maintain profitability amidst rising operational costs. This environment has opened doors for FinTech firms that leverage technology to offer lower fees and enhanced user experiences. For instance, companies like Square and PayPal have seen exponential growth in their user bases as they provide seamless transaction processes that appeal particularly to younger demographics.

Market Dynamics: Inflation and Interest Rates

The macroeconomic backdrop plays a crucial role in shaping investor sentiment towards FinTech stocks. With inflationary pressures mounting—recently reported at 5% year-on-year—central banks are contemplating tightening monetary policy sooner than expected. Such moves could impact liquidity in the markets, affecting both consumer spending and investment flows into tech sectors.

As highlighted by CNBC, higher interest rates may initially pose challenges for growth-oriented sectors like FinTech; however, they can also create an environment ripe for consolidation among smaller players unable to withstand increased borrowing costs. Investors should closely monitor these dynamics as they unfold, particularly during earnings season when companies report on their performance amid changing economic conditions.

The Rise of AI-Driven Financial Solutions

Artificial intelligence (AI) is becoming a cornerstone of innovation within the FinTech space. Companies utilizing AI algorithms can analyze vast amounts of data quickly, providing personalized financial advice or risk assessments that were previously unattainable at scale. According to Reuters, firms integrating AI into their operations have reported improved customer retention rates and reduced fraud incidents—a critical factor as cyber threats continue to escalate.

This technological advancement not only enhances operational efficiency but also positions these companies favorably against traditional banks that may lag in adopting such innovations. As more consumers seek tailored financial products, those investing in AI-driven FinTech solutions may find themselves ahead of the curve.

Investment Opportunities Amidst Industry Disruption

The intersection of FinTech innovation with evolving consumer preferences presents unique investment opportunities within the U.S. stock market. Exchange-traded funds (ETFs) focusing on technology-driven financial services have gained traction among retail investors seeking exposure without picking individual stocks directly. These ETFs often include major players like Visa and Mastercard alongside emerging disruptors like Robinhood or Chime.

Moreover, as regulatory frameworks evolve around cryptocurrencies and decentralized finance (DeFi), savvy investors might consider diversifying their portfolios with exposure to blockchain technologies or crypto-related equities—areas poised for substantial growth given increasing institutional adoption.

A Cautious Outlook: Risks Ahead

Despite the promising outlook for FinTech investments, potential risks cannot be overlooked. Regulatory scrutiny is intensifying globally; any missteps could lead to significant penalties or operational restrictions impacting profitability margins across the sector. Additionally, heightened competition from both established banks pivoting towards digital offerings and new entrants could compress margins further.

I’ve observed phases where investor enthusiasm wanes despite strong fundamentals due to broader market anxieties surrounding inflation or geopolitical tensions—factors that can lead even resilient sectors like FinTech into turbulent waters if not managed carefully.

Conclusion: Preparing for Change

The digital banking revolution is not merely a trend; it represents a fundamental shift in how financial services will operate moving forward. For investors aged 25-45 who have navigated through several market cycles over the past decade, understanding this transformation will be key in adapting strategies accordingly.

As we approach this pivotal moment characterized by rapid technological advancements intertwined with macroeconomic shifts, staying informed about industry developments will empower you to make strategic decisions aligned with your long-term goals.